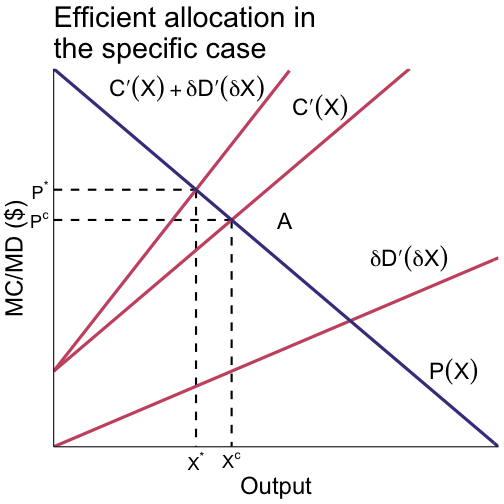

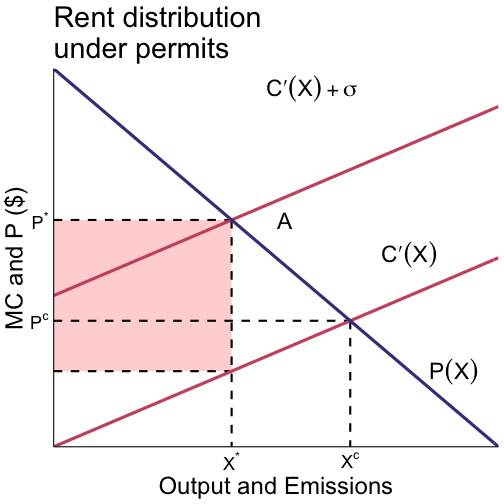

class: center, middle, inverse, title-slide # Lecture 5 ## Competitive output markets ### Ivan Rudik ### AEM 6510 --- exclude: true ```r if (!require("pacman")) install.packages("pacman") pacman::p_load( tidyverse, tidylog, xaringanExtra, rlang, patchwork ) options(htmltools.dir.version = FALSE) knitr::opts_hooks$set(fig.callout = function(options) { if (options$fig.callout) { options$echo <- FALSE } knitr::opts_chunk$set(echo = TRUE, fig.align="center") options }) ``` ``` ## Warning: 'xaringanExtra::style_panelset' is deprecated. ## Use 'style_panelset_tabs' instead. ## See help("Deprecated") ``` ``` ## Warning in style_panelset_tabs(...): The arguments to `syle_panelset()` changed in xaringanExtra 0.1.0. Please refer ## to the documentation to update your slides. ``` --- # Roadmap So far we have ignored output markets in our analysis -- But firms actually have production costs in addition to abatement costs, and sometimes these costs cannot be disentangled -- Now we explore models where output and abatement may not be separable This captures a wider range of potential abatement methods and technologies --- # The competitive output model This model is simply an extension of our previous one For now drop firm-specific subscripts but we assume firms are asymmetric -- A firm's production technology is given by: `$$x = f(l_1,\dots,l_K)$$` where `\(x\)` is how many units of output are produced using production function `\(f\)` and vector of inputs `\(\{l_1,\dots,l_K\}\)` --- # The competitive output model A firm's emission technology is given by: `$$e = g(l_1,\dots,l_K)$$` where `\(e\)` is how many units of emissions resulting from using the vector of inputs `\(\{l_1,\dots,l_K\}\)` -- Note that the marginal product of `\(l_k\)` for either `\(f\)` or `\(g\)` could be positive, negative, or zero -- Why? -- An input that reduces emissions could reduce output, output-enhancing inputs could increase emissions or be emission-neutral --- # The competitive output model Next we need the cost functions -- The cost function `\(C(x,e)\)` is derived from the firm's cost minimization problem -- We want to minimize the costs of producing a given combination of output `\((x,e)\)` `$$C(x,e) = \min_{l_1,\dots,l_k} \left\{ \sum_{k=1}^K w_k l_k + \lambda \underbrace{\left[ x - f(l_1,\dots,l_K) \right]}_{\text{x units of output}} + \mu \underbrace{\left[e-g(l_1,\dots,l_K)\right]}_{\text{e units of emissions}} \right\}$$` where `\(\{w_1,\dots,w_K\}\)` is a vector of input prices --- # The competitive output model Let `\(\hat{e}^x\)` be the freely chosen level of emissions at output level `\(x\)` We need two sets of assumptions to continue -- ## Assumption Set 1 .hi-red[(general case)] -- 1. `\(C(x,e)\)` is twice continuously-differentiable with `\(C_x > 0\)` and for any `\(x\)` there is an emission level `\(\hat{e}^x\)` such that `\(C_e(x,\hat{e}^x) = 0\)` -- 2. `\(C_e(x,\hat{e}^x) < 0 \,\,\, \forall e < \hat{e}^x\)` and `\(C_e(x, \hat{e}^x) \geq 0 \,\,\, \forall e \geq \hat{e}^x\)` -- 3. `\(C_{xe} = C_{ex} < 0 \,\,\, \forall e < \hat{e}^x\)` -- 4. `\(C_{xx} > 0, C_{ee} > 0, C_{xx}C_{ee} - C_{ex}^2 > 0\)` --- # The competitive output model What do these tell us? 1. MC of production is positive and there is a cost-minimizing emission level `\(\hat{e}^x\)` for all `\(x\)` in the absence of environmental regulation -- 2. MAC is increasing in abating below `\(\hat{e}^x\)` -- 3. MC of production is smaller with higher emissions `\(\leftrightarrow\)` MAC shifts up if output rises -- 4. Production and abatement costs are convex (marginal costs are increasing) --- # The competitive output model We can also see that the non-regulated emission level `\(\hat{e}^x\)` rises with `\(x\)` from the `\(C_e(x,\hat{e}^x) = 0\)` assumption -- Differentiate `\(C_e(x, \hat{e}^x) = 0\)` wrt `\(x\)` to get: `\(C_{ex}(x,\hat{e}^x){dx \over dx} + C_{ee}(x,\hat{e}^x){d\hat{e}^x \over dx} = 0\)` -- Rearrange to get: `\({d\hat{e}^x \over dx} = - {C_{ex} \over C_{ee}} > 0\)` --- # The competitive output model ## Assumption Set 2 .hi[(specific case)] We will be directly linking emissions to output in the .hi[specific case] so we make these assumptions: - Cost function `\(C(x)\)` is twice continuously-differentiable -- - `\(C'(x) > 0, C''(x) > 0\)` -- - Emissions are given by `\(e = \delta(x)\)` where `\(\delta'(x) > 0\)` -- - In some cases we will assume `\(\delta(x) = \delta \cdot x\)` to simplify --- # The competitive output model What do these tell us? The MAC function is tired directly to the firm's marginal profit -- If `\(p\)` is the output price of `\(x\)`, profit is: `$$\Pi = px - c(x)$$` and if `\(e = \delta x\)` we have that: `$${d \Pi \over de} = {p - C'(e/\delta) \over \delta}$$` --- # The competitive output model At an unregulated optimum it must be that `\(p - C'(x) = 0\)` so `\(p - C'(\hat{e}^x/\delta) = 0\)` defines the unregulated level of emissions -- For `\(e < \hat{e}^x\)`: `\(p - C'(e/\delta) > 0\)` since `\(\hat{e}^x\)` is privately optimal for the firm -- Thus `\({d \Pi \over de}\)` is the marginal abatement cost where `\({d \Pi \over de} > 0\)` for `\(e < \hat{e}^x\)` -- .hi-blue[The MC of abatement is the forgone marginal profits from reducing emissions] -- We can also see that the MAC is increasing: `$${d^2 \Pi \over de^2} = {C''(e/\delta) \over \delta^2} \geq 0$$` --- # The competitive output model Next we need to model the demand side of the market -- Let consumer utility be: `$$U^i = U_i(x_i) + z_i - D_i(E)$$` where - `\(x_i\)` is the person's consumption level - `\(z_i\)` is spending on all other non- `\(x\)` goods - `\(D_i(E)\)` are damages from aggregate emissions `\(E\)` - There are `\(i=1,\dots,J\)` consumers --- # The competitive output model The consumer has a budget constraint: `$$y = px_i + z_i$$` where the price of `\(z_i\)` is normalized to 1, `\(p\)` is the price of `\(x\)` in terms of `\(z\)` -- Utility maximization gives us that `\(u'_i(x_i) = p\)` -- This defines the inverse demand for `\(x\)` as: `\(p_i(x_i) = u'_i(x_i)\)` -- We can then derive gross benefits from consumption: `\(\int_0^{x_i} u'_i(s)ds = u_i(x_i)\)` --- # The competitive output model Next we want to derive .hi-blue[aggregate] market benefits -- Let `\(X = \sum_{i=1}^I x_i\)` be aggregate consumption, `\(P(X)\)` be the market inverse demand curve, and `\(D(E)\)` be the aggregate damage curve - You get `\(P(X)\)` by just horizontally summing `\(p_i(x_i)\)` like we did in previous classes -- `\(P(X)\)` and `\(D(E)\)` allow us to .hi-blue[fully] characterize benefits and damages to households --- # The competitive output model Now we have both sides of our model, next we need to define .hi-blue[social welfare] so we can find efficient outcomes -- Social welfare in the .hi-red[general case] is given by: `$$W(x_1,\dots,x_J,e_1,\dots,e_J) \equiv \int_0^{X\equiv\sum x_j} P(s)ds - \sum_{j=1}^J C^j(x_j, e_j) - D(E)$$` where `\(j\)` are specific firms, and household costs and firm revenues cancel out because they are just a transfer from households to firms Welfare is CS minus total cost, minus damages --- # The competitive output model Social welfare in the .hi[specific case] when `\(e_j = \delta_j(x_j)\)` is given by: `$$W(x_1,\dots,x_J) \equiv \int_0^{X\equiv\sum x_j} P(s)ds - \sum_{j=1}^J C^j(x_j) - D(E)$$` where `\(E = \sum_{j=1}^J \delta_j(x_j)\)` -- Now we can derive the efficiency conditions for our model to understand what defines the optimal allocation --- # The competitive output model: Efficiency Begin with the .hi-red[general case], the FOCs are defined by: `$${\partial W\over\partial x_j} = P(X) - C^j_{x_j}(x_j, e_j) = 0\rightarrow P(X) = C^j_{x_j}(x_j, e_j)$$` where `\({\partial \over \partial x_j} \int_0^{X\equiv\sum x_j} P(s)ds = P(X) {\partial X \over \partial x_j} = P(X)\)` by the fundamental theorem of calculus, -- and -- `$${\partial W\over\partial e_j} = C^j_{e_j}(x_j,e_j) + D'(E) = 0 \rightarrow D'(E) = -C^j_{e_j}(x_j,e_j)$$` These `\(2J\)` equations give us the solutions `\(x^*_j, e^*_j\)` for `\(j=1,\dots,J\)` --- # The competitive output model: Efficiency The conditions are pretty straightforward, right? -- - `\(P(X) = C^j_{x_j}(x_j, e_j)\)` tells us that marginal benefit of consumption must equal marginal cost of consumption -- - `\(-C^j_{e_j}(x_j,e_j) = D'(E)\)` tells us that marginal abatement cost must equal marginal damage -- For efficiency, we need to balance the environmental and production costs of producing the good with the benefits of consuming it --- # The competitive output model: Efficiency The .hi[specific case] can give us some more insight -- Here only the `\(x_j\)`s are choice variables so we get the following FOCs: `$$P(X) = C'_j(x_j) + D'(E)\delta_j'(x_j) \,\,\,\, j=1,\dots,J$$` -- The left hand side is the marginal benefit of consumption -- The right hand side is the total marginal cost: - Private production costs - External damage costs --- # Efficiency in the specific case .pull-left[  ] .pull-right[ `\(X^c\)` is the competitive allocation, this results in: - Too much production - Too low of an output price `\(X^*\)` is the optimal allocation where SMB = SMC - This results in less production than the competitive allocation at a higher price ] --- # Efficiency in the specific case .pull-left[  ] .pull-right[ Where do the aggregate curves come from? We get aggregate private MC `\(C'(X) = \sum_{j=1}^J C'_j(x_j)\)` by *horizontally* summing firm MCs We get SMC by *vertically* summing PMC and MD ] --- # Policy instruments Now we will take another look at our environmental policy instruments in this model with output markets -- We will see that: -- - There are additional results related to the output market that we didn't have before -- - The previous results all still hold: taxes, subsidies, permits can all achieve the efficient allocation --- # Policy instruments: taxes When facing an emission tax `\(\tau\)` a competitive firm's problem in the .hi-red[general case] is: `$$\Pi_j(x_j, e_j) = p x_j - C^j(x_j,e_j) - \tau e_j$$` where `\(p\)` is the market price of `\(x\)` -- The firm's FOCs are: -- `\begin{align} p &= C'_{x_j}(x_j,e_j) \\ \tau &= -C'_{e_j}(x_j,e_j) \end{align}` --- # Policy instruments: taxes The firm's FOCs are: `\begin{align} p &= C'_{x_j}(x_j,e_j) \\ \tau &= -C'_{e_j}(x_j,e_j) \end{align}` -- The firm equates MR to MC of production -- The firm equates the marginal abatement cost to the tax level -- So if the regulator sets `\(\tau = D'(E^*)\)` .hi-blue[we can achieve the efficient allocation] --- # Policy instruments: taxes When facing an emission tax `\(\tau\)` a competitive firm's problem in the .hi[specific case] where `\(e_j = d x_j\)` is: `$$\Pi_j(x_j) = p x_j - C^j(x_j) - \tau \delta x_j$$` with FOC: `$$p = C'_j(x_j) + \tau \delta$$` -- If the regulator sets `\(\tau = D'(E^*)\)` then firms behave as if `$$P(X) = C'_j(x_j) + \delta D'(E^*)$$` .hi-blue[which matches our social efficiency condition] --- # Comparative statics Now that we have an output market in our model we can study how taxes influence it -- To start we will assume all firms are identical and we are in the .hi[specific case] of the model so our profit-maximizing firm FOC is: `$$P(X) = C'(x) + \delta\tau$$` where `\(X = x\cdot J\)` -- Differentiate the FOC with respect to `\(\tau\)` to get how output and emissions respond to a change in the tax rate --- # Comparative statics Differentiating gives us: `$$\left[P'(X)J - C''(x)\right]{dx \over d\tau} = \delta$$` which implies that: `$${dx\over d\tau} = {\delta \over P'(X)J - C''(x)} < 0$$` and `\({dX\over d\tau} = J{dx\over d\tau} < 0\)` Emission taxes reduce output --- # Comparative statics With `\(E = \delta \cdot X\)` we have how emissions respond to the tax: `$${dE\over d\tau} = J \delta {\delta \over P'(X)J - C''(x)} < 0$$` and since `\(p = P(X)\)` is the market price of output, we can determine the relationship between output prices and the tax: `$${dp\over d\tau} = P'(X){d X \over d\tau} > 0$$` --- # Comparative statics Recap: What do the comparative statics tell us? Output and emissions decline in the tax: - A tax on emissions raises the marginal cost of production for firms - Supply shifts left - Output price `\(p\)` goes up, quantity `\(x\)` goes down --- # Comparative statics The .hi-blue[incidence] of the tax is also made clear by: `$${dp\over d\tau} = P'(X){d X \over d\tau} > 0$$` Incidence is how the tax burden is distributed between consumers and producers -- The more the price of `\(x\)` increases in response to a tax, the more the consumers pay for `\(x\)` because of `\(\tau\)`, the higher their tax incidence -- Recall from Econ 101 that it doesn't matter who is taxed, the burden is shared by the consumers and producers --- # Comparative statics `$${dp\over d\tau} = P'(X){d X \over d\tau} > 0$$` If `\(P'(X)\)` is small, demand is .hi-blue[elastic (flat)], and consumers have low incidence because the price they pay does not change much in the tax, firms bear most of the cost of the tax -- If demand is perfectly elastic `\(P'(X) = 0\)` and there is no associated price increase from a tax increase --- # Comparative statics `$${dp\over d\tau} = P'(X){d X \over d\tau} > 0$$` If `\(P'(X)\)` is large, demand is .hi-blue[inelastic (steep)], and consumers have high incidence because the price they pay for `\(x\)` increases substantially in the tax, firms pass-through most of the tax to consumers -- If demand is perfectly inelastic, then consumers bear the entire cost of the tax --- # Comparative statics: taxes recap What did we learn? Increasing a tax: 1. Decreases firm and aggregate emission levels 2. Decreases firm and aggregate output (even in the general case, see pg 103-104 in the book) 3. Increases output prices --- # Policy instruments: permits Now suppose the regulator issues `\(L=E^*\)` permits instead of setting a tax -- The regulator knows that the permit price `\(\sigma\)` that clears the permit market will be `\(\sigma(L) = \sigma(E^*) = D'(E^*)\)` -- Similarly, the output price will then be `\(p = P(X^*)\)` -- The regulator can achieve the first-best efficient outcome --- # Policy instruments: permits Auctioned versus freely-distributed permits are equivalent in this model in terms of .hi-blue[efficiency] -- The permit price in the market under free distribution will match the price that clears the permit auction -- Output prices will also be the same because all firm and consumer decisions will be identical -- The one way they will be different is how the .hi-blue[rents (economic profits)] are distributed: who gets the value from the scarcity of permits, the firms or the government? --- # Distribution of rents in permit markets .pull-left[  ] .pull-right[ Assume `\(x = \delta e\)` and `\(\delta=1\)` so we can plot them on the same scale The red shaded area is the rents from the permit scheme If freely allocated: they remain with firms If auctioned: they go to the government as revenue ] --- # Relative/intensity standards A common form of standards is called a .hi-red[relative standard] -- Relative standards regulate firms based on the concentration of pollution relative to some measurable output -- A relative standard would look something like: $$ e/x \leq \alpha$$ or equivalently: `\(e \leq \alpha x\)` where `\(\alpha\)` is the policy variable -- Relative standards are often called intensity standards because `\(e/x\)` measures the pollution intensity of output --- # Relative/intensity standards Relative standards are only interesting in the .hi-red[general case] of our model, in the .hi[specific case]: - If `\(\delta > \alpha\)`, the firm has to shut down - If `\(\delta \leq \alpha\)`, the firm complies with the regulation no matter its actions -- Assume the regulation is binding in the .hi-red[general case] (i.e. it actually affects firm behavior), then the firm will always set `\(e = \alpha x\)`<sup>1</sup> .footnote[ <sup>1</sup>Choosing `\(e\)` strictly less than `\(\alpha x\)` strictly raises costs and reduces profits. ] This lets us re-write a firm's profit function as: `\(\Pi(x) = px - C(x, \alpha x)\)` --- # Relative/intensity standards `$$\Pi(x) = px - C(x, \alpha x)$$` -- If the regulation is binding, the firm really is only choosing one variable, `\(x\)` -- The FOC is: `$$p = C_x(x,\alpha x) + \alpha C_e(x, \alpha x)$$` The implicit solution to this, `\(x(\alpha)\)`, is the firms supply function, dependent on the policy `\(\alpha\)` --- # Relative standards vs quantity standards Suppose the regulator wants to hit `\(e = \bar{e}\)` and she knows `\(x(\alpha)\)` All the regulator has to do is set `\(\alpha = \bar{e}/x(\alpha)\)` -- Now suppose the firm just uses a quantity standard and directly sets `\(e = \bar{e}\)` -- The firm's profit function is: `$$\Pi(x,\bar{e}) = px - C(x,\bar{e})$$` and the firm's supply `\(x(\bar{e})\)` is defined by `\(p = C_x(x,\bar{e})\)` -- If the regulator chooses `\(\bar{e} = e^*\)` the regulator can achieve the efficient outcome --- # Relative standards vs quantity standards Recall the relative standard FOC if we wanted to set `\(e = \bar{e}\)`: `$$p = C_x(x(\alpha),\bar{e}) + \alpha C_e(x(\alpha), \bar{e})$$` -- and notice that this means that: `$$p - \alpha C_e(x(\alpha), \bar{e}) = C_x(x(\alpha), \bar{e}) > p$$` since `\(-C_e\)` is positive -- What does this mean? --- # Relative standards vs quantity standards This means that: `$$C_x(x(\alpha), \bar{e}) > C_x(x(\bar{e}), \bar{e})$$` -- It follows pretty simply that: `\(x(\alpha) > x(\bar{e})\)` and that: -- - `\(C(x(\alpha), \bar{e}) > C(x(\bar{e}), \bar{e})\)` since `\(C_{xx} > 0\)` -- - `\(-C_e(x(\alpha), \bar{e}) > -C_e(x(\bar{e}), \bar{e})\)` since `\(C_{ex} < 0\)` -- .hi-blue[Total cost and marginal production and abatement costs are higher under a relative standard] --- # Relative standards vs quantity standards Takeaways: If a regulator sets an emission goal of `\(\bar{e}\)` for a single firm or `\(J\)` firms, then a relative standard will lead to: -- - higher output -- - higher total cost -- - higher marginal abatement cost relative to a quantity standard -- Why? --- # Relative standards vs quantity standards How can the firm achieve compliance under a relative standard `\((e/x \leq \alpha)\)`? -- Two ways: -- 1. Decrease emissions `\(e\)` -- 2. Increase output `\(x\)` -- Relative standards allow the firm to meet the standard *in ways we don't want them to,* so we end up with too much output This limits us to .hi-blue[second-best] outcomes --- # Relative standards: optimal policy If we need to use a relative standard due to political or technical reasons what standard should we set to maximize welfare? -- The regulator's problem is: `$$W(\alpha) = \int_{0}^{x(\alpha)} P(t) dt - C(x(\alpha), \alpha x(\alpha)) - D(\alpha x( \alpha))$$` -- The FOC is: `$$[P - C_x - \alpha C_e] x'(\alpha) - C_e x - D' \times [x + \alpha x'(\alpha)] = 0$$` where the term in the first bracket is 0 from the firm's `\(\pi\)`-max FOCs --- # Relative standards: optimal policy This gives us that: `$$- C_e ={x + \alpha x'(\alpha) \over x } D'$$` .hi-blue[This is not MAC = MD!] -- `\(x'(\alpha)\)` tells us how output responds to policy and its sign tells us whether MAC `\(>\)` MD or vice versa -- Suppose `\(x'(\alpha) > 0\)`, then the second best policy sets MAC `\(>\)` MD: - The second-best quantity of emissions is lower than the first-best / optimal level that sets MAC = MD --- # Environmental policy in the long run So far we have assumed a fixed number of firms `\(J\)` In the long run, firms may enter or exit the market, and this may affect the efficiency properties of our policies -- Econ 101 tells us that in perfectly competitive markets: -- - Firms are identical -- - Firms enter or exit until profits are driven to zero -- - Firms produce at minimum average cost -- - Optimal number of firms is endogenous (usually) -- We will now look at long run properties of policy with identical firms --- # Environmental policy in the long run In the long run, firms have fixed and variable costs: `\begin{align} C(x,e) = \begin{cases} VC(x,e) + F \text{ if } x,e \neq 0 \\ 0 \text{ if } x,e = 0 \end{cases} \\ \end{align}` where `\(F\)` is the fixed cost of entry, and `\(VC\)` denotes variable costs of operation -- In the long run, social welfare will depend on `\(x,e\)` .hi-blue[and the number of firms] `\(J\)` --- # Environmental policy in the long run Social welfare is given by: `$$W(x,e,J) = \max_{x,e,J} \int_0^{x\cdot J} P(t) dt - J\cdot C(x,e)-D(e\cdot J)$$` -- The FOCs for a social optimum are: `\begin{align} P(X^*) =& C_x(x^*,e^*) \tag{x FOC} \\ D'(E^*) =& -C_e(x^*,e^*) \tag{e FOC} \\ P(X^*)x^* =& C(x^*,e^*) + D'(E^*)e^* \tag{J FOC} \end{align}` The last expression is the new one for .hi[long-run efficiency] --- # Environmental policy in the long run With some slight rearranging of the `\(J\)` FOC we can get: `$$P(X^*) = { C(x^*,e^*) + D'(E^*)e^*\over x^*}$$` What does this say? -- First, for a small firm: -- `\(D'(E^*)e^*\)` is approximately the damage caused by that firm because -- for sufficiently small `\(e^*\)`, `\(D'(E^*)\)` will be approximately constant `\((\delta)\)` (by a Taylor expansion argument) --- # Environmental policy in the long run With some slight rearranging of the `\(J\)` FOC we can get: `$$P(X^*) = \underbrace{{C(x^*,e^*) + \delta e^*\over x^*}}_{\text{average social cost}}$$` This means that it is socially efficient for firms to enter or exit until the price of output (approximately) equals the .hi-blue[average social cost curve] --- # Standards in the long run In the short run we had that standards were equivalent to taxes and tradable permits Is this true in the long run? -- Suppose the regulator wants to cap total emissions at `\(E^*\)` -- She sets an emission standard `\(e^* = E^*/J^*\)` for all firms where `\(J^*\)` is the optimal long run number of firms -- Firms can now only choose `\(x\)` since `\(e\)` is fixed at `\(e^*\)` --- # Standards in the long run Firms choose output according to: `$$p = C_x(x,e^*)$$` -- In the long run competitive equilibrium we will have `\(\hat{J}\)` firms all producing `\(\hat{x}\)` units of output such that: -- `\begin{align} &P(\hat{x}\hat{J}) = C_x(\hat{x},e^*) \tag{MR = MC}\\ &P(\hat{x}\hat{J})\hat{x} - C(\hat{x},e^*) = 0 \tag{Zero Profit} \end{align}` -- MR = MC, and zero profits are our two equilibrium conditions -- MR = MC maximizes firm profit, zero profits ensures no change in # of firms --- # Standards in the long run Recall that long run efficiency required that: `$$P(X^*)x^* - C(x^*,e^*) = D'(E^*)e^* > 0$$` -- so we have that `\(\hat{J} \neq J^*\)` and `\(\hat{x} \neq x^*\)`! What's the intuition? -- When we impose a standard: -- 1. Firms cut back output -- 2. This raises (short-run) profit above zero -- 3. Firms enter the market until profits go to zero: so `\(\hat{J} > J^*\)` and we will have that `\(\hat{x} < x^*\)` --- # Standards in the long run This is important! -- Conventional wisdom tells us that taxes, permits, and standards can all achieve the efficient outcome -- This is only true in the short run -- In the long run: standards do not appropriate the damage to the environment `\(D'(E^*)e^*\)` from firms, so we get .hi-red[excess entry] and standards are no longer first-best --- # Taxes in the long run Can taxes achieve the efficient outcome in the long run? -- Yes and it is pretty easy to see, suppose the regulator sets a tax of: `$$\tau = D'(E^*)$$` -- Firm profit is then: `$$\Pi = px - C(x,e) - \tau e$$` -- Giving us FOCs: `$$p = C_x(x^*,e^*) \qquad -C_e(x^*,e^*) = \tau$$` --- # Taxes in the long run In the long run firms enter until profits are zero so: `$$\Pi = P(X^*)x^* - C(x^*,e^*) - \tau e^* = 0$$` so `\(\tau = D'(E^*)\)` implies that `$$P(X^*)x^* = C(x^*,e^*) + D'(E^*)e^*$$` The firm FOCs for production and the entry zero-profit condition map exactly to the social welfare maximizing conditions! -- The payment of tax rents from the firms to the regulator of `\(\tau e^* = D'(E^*)e^*\)` limits entry and is what makes taxes efficient in the long run --- # Permits in the long run Now what about permit systems? -- Suppose the regulator auctions off `\(L=E^*=e^*J\)` permits and let `\(\sigma\)` be the market-clearing permit price -- The long run equilibrium is defined by the two firm FOCs and the entry condition: `\begin{align} &P(x^*J) = C_x(x^*,e^*) \\ &\sigma = -C_e(x^*,e^*) \\ &P(x^*J)x^* - C(x,e) - \sigma e^* = 0 \end{align}` --- # Permits in the long run -- Similar to the short run we will have that `\(\sigma = -C_e(x^*,e^*) = D'(L) = D'(E^*)\)` -- Thus the three long run efficiency conditions are satisfied again if we auction off the permits: - MR = MC - MAC = MD - P = ASC -- Now what if we freely distribute permits? What do you think? -- It seems like it might not be long run efficient: -- firms are not paying the environmental rent, so zero profit and P = ASC might not occur --- # Permits in the long run Suppose we allocate `\(\bar{e}\)` permits to the .hi-[incumbent] identical firms, profit for the incumbent firms given permits is then: `$$\Pi = px - C(x,e) - \sigma(e-\bar{e})$$` -- and profit for any future entrants who were not given an allocation is: `$$\Pi = px - C(x,e) - \sigma e$$` What two things do you notice? -- First, for any given `\(\sigma\)`, entrants and incumbents cannot both have zero profit! -- Our P = ASC condition can't hold for all firms --- # Permits in the long run Our efficiency condition is now .hi-red[new firms enter until profits are zero (P=ASC for entrants)]: `$$\Pi = px - C(x,e) - \sigma e = 0$$` so that incumbent firms sustain long run profits of: `$$\sigma\bar{e}$$` -- What is this saying? -- .hi-blue[Operating profits] of any firms in the market are zero, incumbents had long run profits **only** from their initial permit allocation --- # Permits in the long run The second thing you should have noticed is that the firm FOCs will be identical to the auctioned permit case, firms face the .hi-blue[exact same] incentives for output and emissions -- This means that freely allocated permits are also long run efficient -- This is just an application of the Coase theorem: the initial assignment of property rights to pollute does not matter for efficiency --- # Subsidies in the long run Now what about subsidies? In the short run they are equivalent to taxes, are they still equivalent in the long run? -- Think about the incentives for entry... -- Denote the reference level of emissions as `\(\hat{e}\)`, firm profits under a subsidy per unit `\(\xi\)` are: `$$\Pi = px - C(x,e) - \xi(e-\hat{e})$$` --- # Subsidies in the long run For damage efficiency we need to set the subsidy equal to MD: `\(\xi = D'(E^*)\)` -- In the long run equilibrium, firms enter until profits are zero `$$\Pi = P(X^*)x^* - C(x^*,e^*) - D'(E^*)(e^*-\hat{e}) = 0$$` -- which implies that `$$P(X^*)x^* - C(x^*,e^*) - D'(E^*)e^* = -D'(E^*)\hat{e} < 0$$` Too many firms have entered! --- # Subsidies in the long run Why did too many firms enter? -- Payments are available to **all** firms and induces excess market entry -- Permits do not have these problems because the payment was only to incumbent firms, not entrants -- Incumbent firms are already in the market: giving them the rents from freely distributed permits does not lead to excess entry