At interior solution, the function must be precisely be zero

Corner solution at the upper bound \(b_i\) for \(x_i\)\(\rightarrow\)\(f\) must be increasing in direction \(i\)

The opposite is true if we are at the lower bound

Complementarity problems

Most economic problems are complementarity problems where we are

Looking for a root of a function (e.g. marginal profit)

Subject to some constraint (e.g. price floors)

The Karush-Kuhn-Tucker theorem shows that \(x\) solves the constrained optimization problem ( \(\max_x F(x)\) subject to \(x \in [a,b]\)) only if it solves the complementarity problem \(CP(f, a, b)\), where \(f_i = \partial F/\partial x_i\)

Let’s use a linear \(f\) to visualize what do we mean by a solution in complementarity problems

Complementarity problems

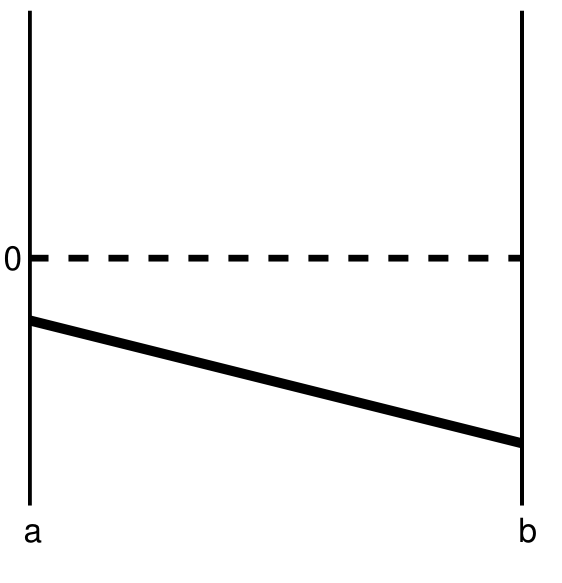

Case 1

What is the solution?

\(x^{*} = a\), with \(f(x^{*}) < 0\)

Another way of seeing it: imagine we’re trying to maximize \(F\)

What would \(F\) look like between \(a\) and \(b\)?

The decreasing part of a concave parabola

Complementarity problems

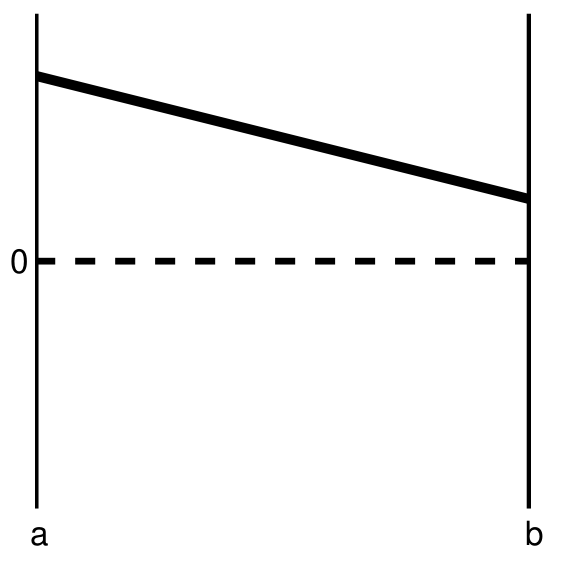

Case 2

What is the solution?

\(x^{*} = b\), with \(f(x^{*}) > 0\)

Once again, imagine we’re trying to maximize \(F\)

What would \(F\) look like between \(a\) and \(b\)?

The increasing part of a concave parabola

Complementarity problems

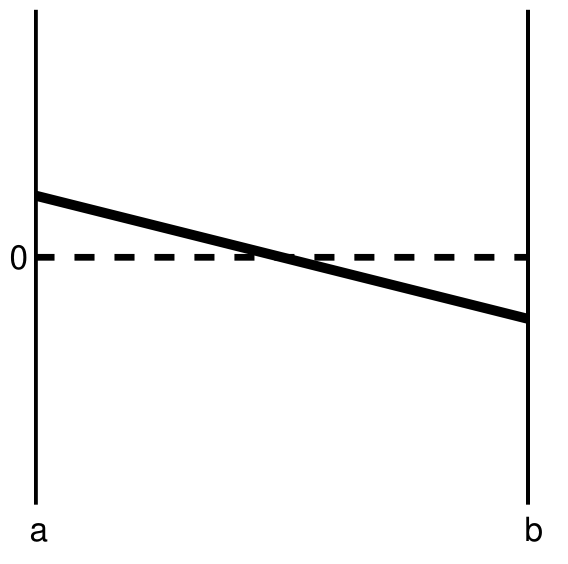

Case 3

What is the solution?

Some \(x^{*}\) between \(a\) and \(b\), with \(f(x^{*}) = 0\)

What would \(F\) look like between \(a\) and \(b\)?

A concave parabola with an interior maximum

Complementarity problems

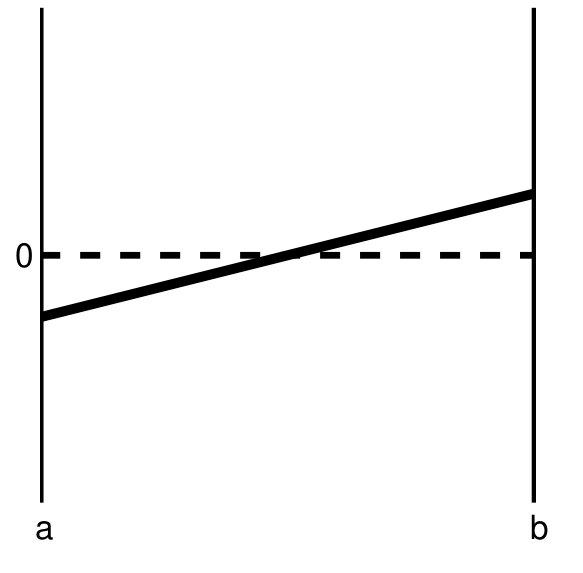

Case 4

What is the solution?

Actually, we have 3 solutions:

\(x^{*} = a\), with \(f(x^{*}) < 0\)

\(x^{*} = b\), with \(f(x^{*}) > 0\)

Some \(x^{*} \in (a,b)\), with \(f(x^{*}) = 0\)

And this is an unstable solution

What would \(F\) look like between \(a\) and \(b\)?

A convex parabola! So we end up with multiple local maxima that satisfy the 1st-order condition

Solving CPs

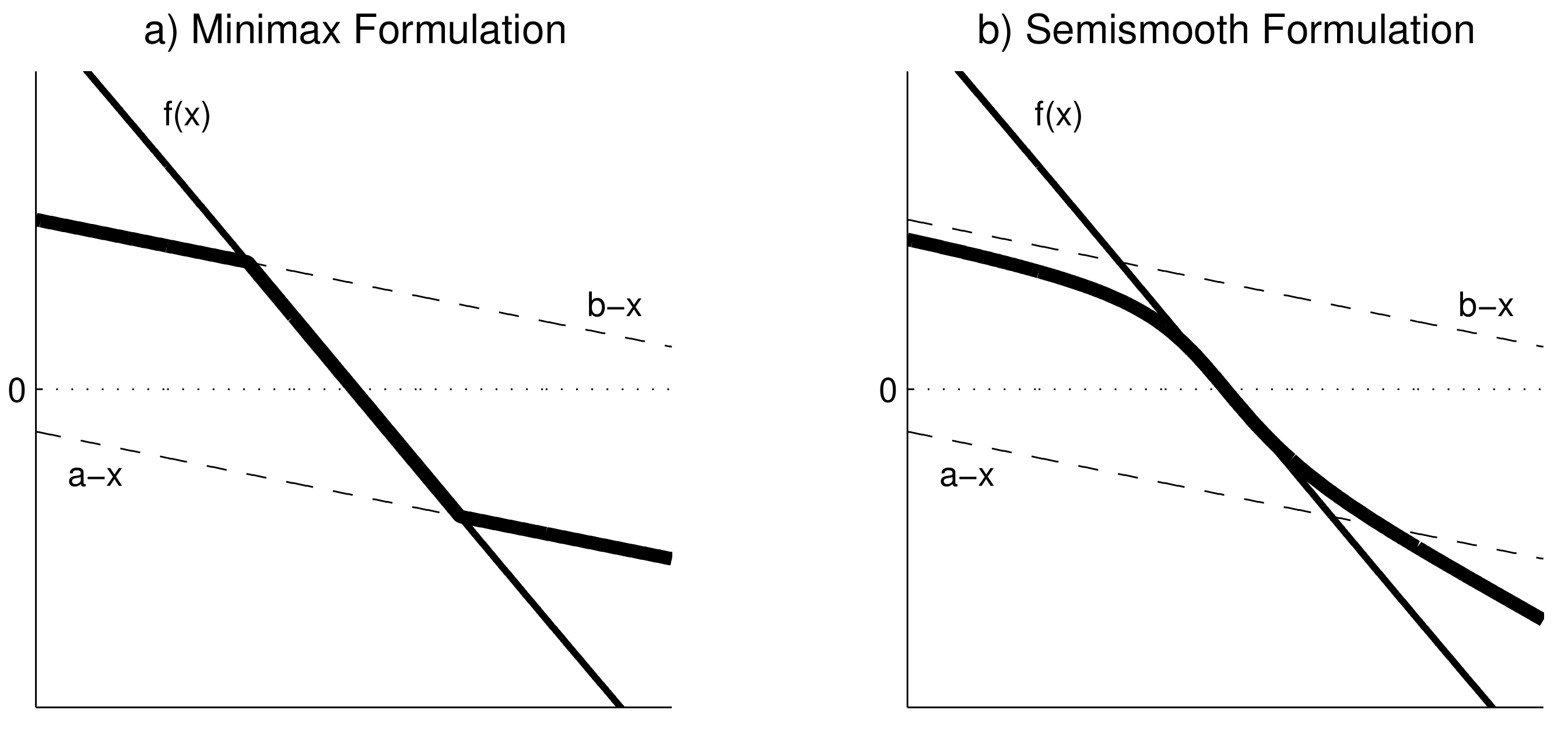

A complementarity problem \(CP(f, a, b)\) can be re-framed as a rootfinding problem

\[

\hat{f}(x) = min(max(f(x),a-x),b-x) = 0

\]

Let’s revisit those 4 cases to understand why this works

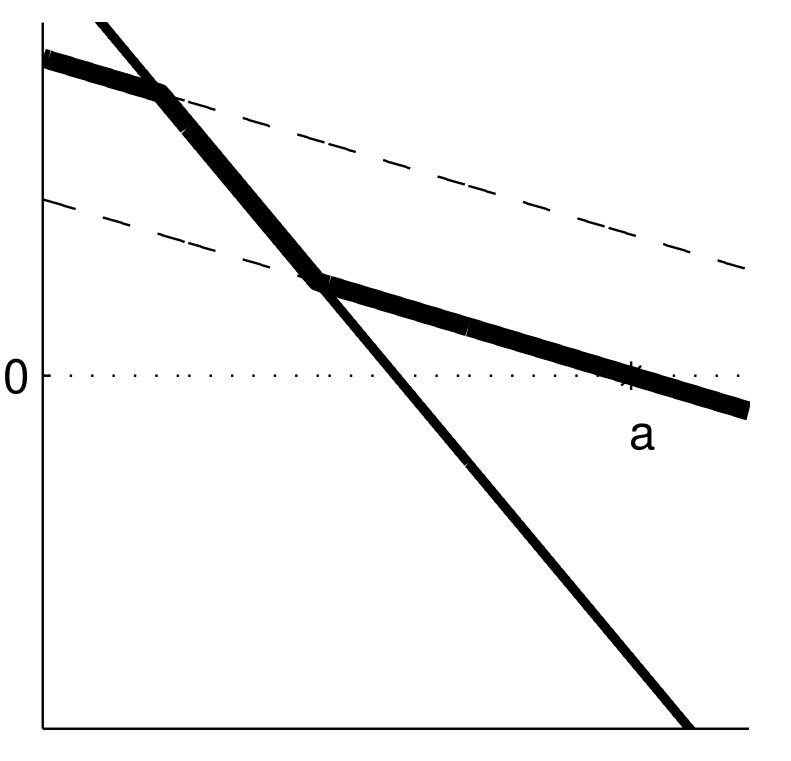

Solving CPs

Case 1

\(\hat{f}(x) = min(max(f(x),a-x),b-x) = 0\)

Dashed lines are \(b-x\) and \(a-x\)

Thin solid line is \(f(x)\)

Thick solid line is \(\hat{f}(x)\)

\(\rightarrow\) The solution is \(x^{*} = a\)

Note that \(f(x) < 0\) for all \(x \in [a,b]\), so this is still case 1

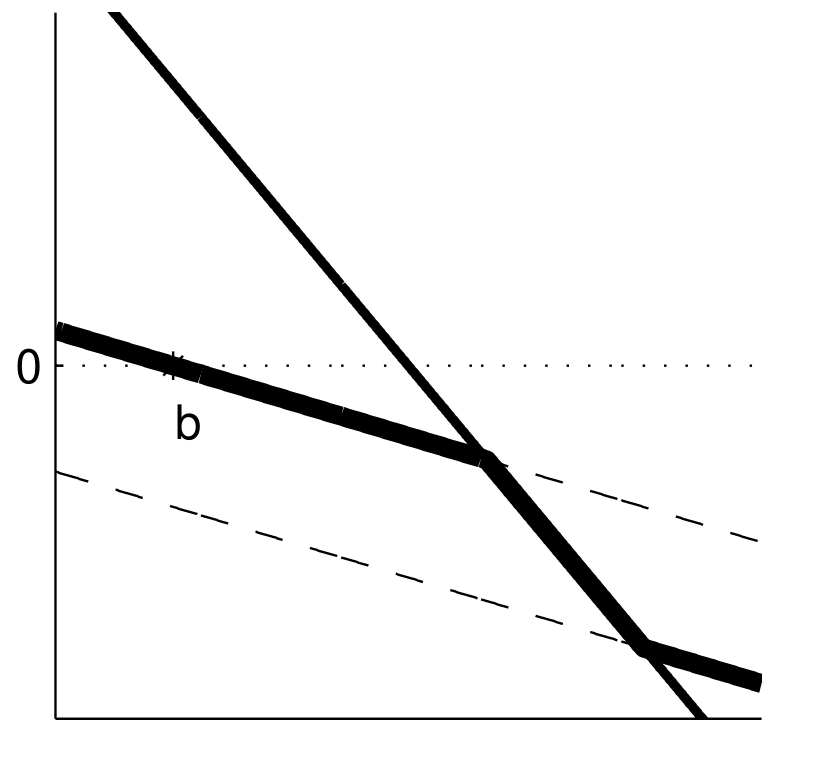

Solving CPs

Case 2:

\(\hat{f}(x) = min(max(f(x),a-x),b-x) = 0\)

In this case, \(f(x) > 0\) for all \(x \in [a,b]\)

\(\rightarrow\) The solution is \(x^{*} = b\)

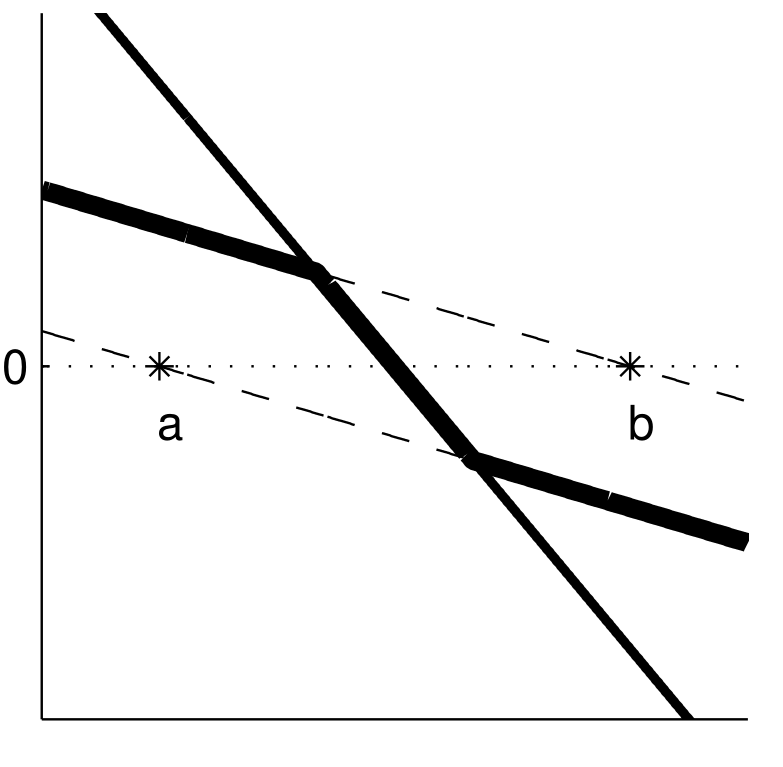

Solving CPs

Case 3:

\(\hat{f}(x) = min(max(f(x),a-x),b-x) = 0\)

In this case, \(f(a) > 0\), \(f(b) < 0\)

\(\rightarrow\) The solution is some \(x^{*} \in (a, b)\)

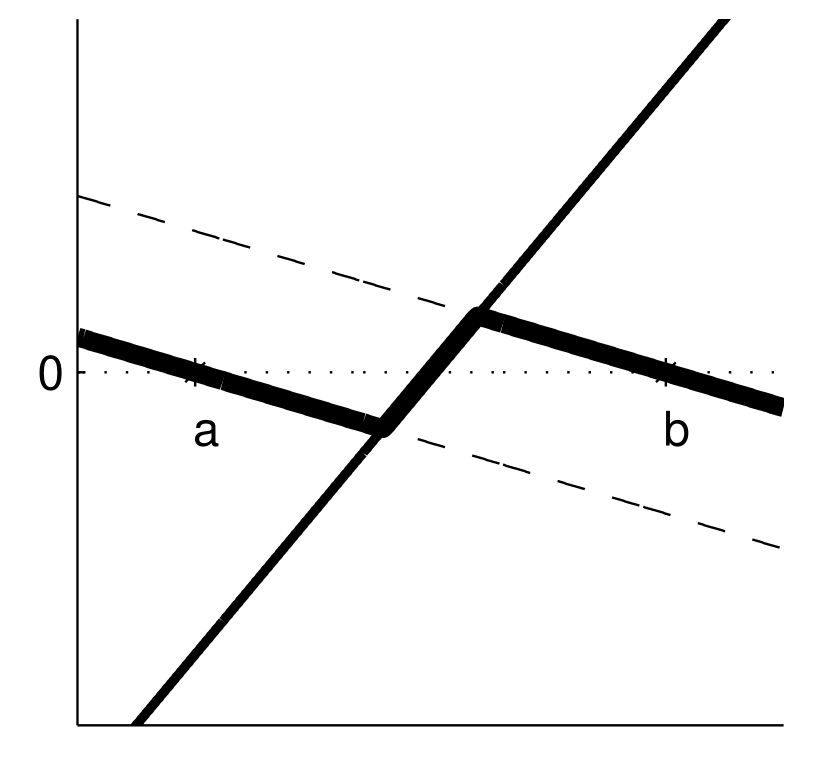

Solving CPs

Case 4:

\(\hat{f}(x) = min(max(f(x),a-x),b-x) = 0\)

In this case, \(f(a) < 0\), \(f(b) > 0\)

\(\rightarrow\) We have the same 3 solutions

\(x^{*} = a\), with \(f(x^{*}) < 0\)

\(x^{*} = b\), with \(f(x^{*}) > 0\)

Some \(x^{*} \in (a,b)\), with \(f(x^{*}) = 0\)

Solving CPs

Once \(\hat{f}\) is defined, we can use Newton’s or quasi-Newton methods to solve a CP

If using Newton, we need to define the Jacobian \(\hat{J}(x)\) with row \(i\) being

functionf!(F, x) # We need to program the memory-efficient version here F[1] =3*x[1]^2+2*x[1]*x[2] +2*x[2]^2+4*x[1] -2 F[2] =2*x[1]^2+5*x[1]*x[2] - x[2]^2+ x[2] +1end;

Solving CPs in Julia

Let’s check the solution to the standard rootfinding problem using Newton’s method

IMPORTANT NOTE. Miranda and Fackler’s textbook (and Matlab package) flip the sign convention for MCP problems. That’s because they are formulating it with an economic context in mind, where these problems arise from constrained optimization.

The conventional setup is (note the flipped inequalities)

But our marginal profit \(f_i > 0\) means the firm wants to increase\(q_i\). At the upper bound \(q_i = K_i\), we expect \(f_i \geq 0\) (wants to produce more but can’t)

The KKT convention has the opposite sign: \(q_i < b_i \Rightarrow f_i \geq 0\), but mcpsolve expects \(f_i \leq 0\)

We need to pass \(-f\) to mcpsolve

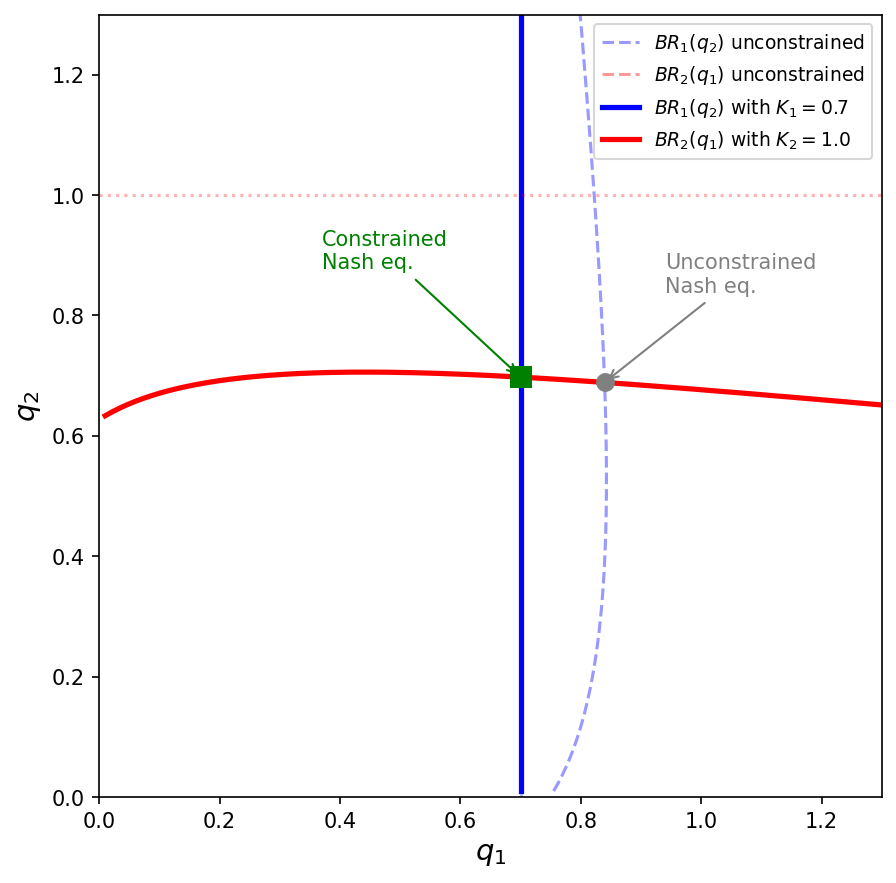

Example: best responses with capacity constraints

Without constraints, the Nash equilibrium is \((q_1^*, q_2^*) \approx (0.84, 0.69)\)

But firm 1 (the low-cost firm) can’t produce more than \(K_1 = 0.7\)!

The constrained equilibrium: \(q_1^* = 0.7\) (at capacity) and \(q_2^* \approx 0.70\) (interior)

Firm 1’s marginal profit is positive at \(q_1 = K_1\): it would produce more if it could

Firm 2’s marginal profit is zero: it is at its unconstrained optimum

This is precisely the complementarity structure: firm 1 is at the upper bound with \(f_1 > 0\), while firm 2 is interior with \(f_2 = 0\)

Example: defining the CP with NLsolve

We define the functions kind of like before, but now using a vector of parameters and flipping the sign convention

epsilon =1.6; c = [0.6; 0.8]; theta =1.0; K = [0.7; 1.0];functionneg_foc!(F, q) Q =sum(q)for i in1:2# NOTE: we flip the sign of f_i to match mcpsolve's convention F[i] =-(theta * Q^(-1/epsilon) - (theta/epsilon) * Q^(-1/epsilon -1) * q[i] - c[i] * q[i])endend

neg_foc! (generic function with 1 method)

Example: solving the CP with NLsolve

usingNLsolvea = [0.0; 0.0]; b = K;r = NLsolve.mcpsolve(neg_foc!, a, b, [0.2, 0.2], method=:newton, autodiff=:forward)

Remember to re-flip the sign of \(f\) to match the KKT convention

F_check =zeros(2); # Create a vector to store the value of f at the solutionneg_foc!(F_check, r.zero); # Compute f at the solutionprintln("f(q*) = $(-F_check)")

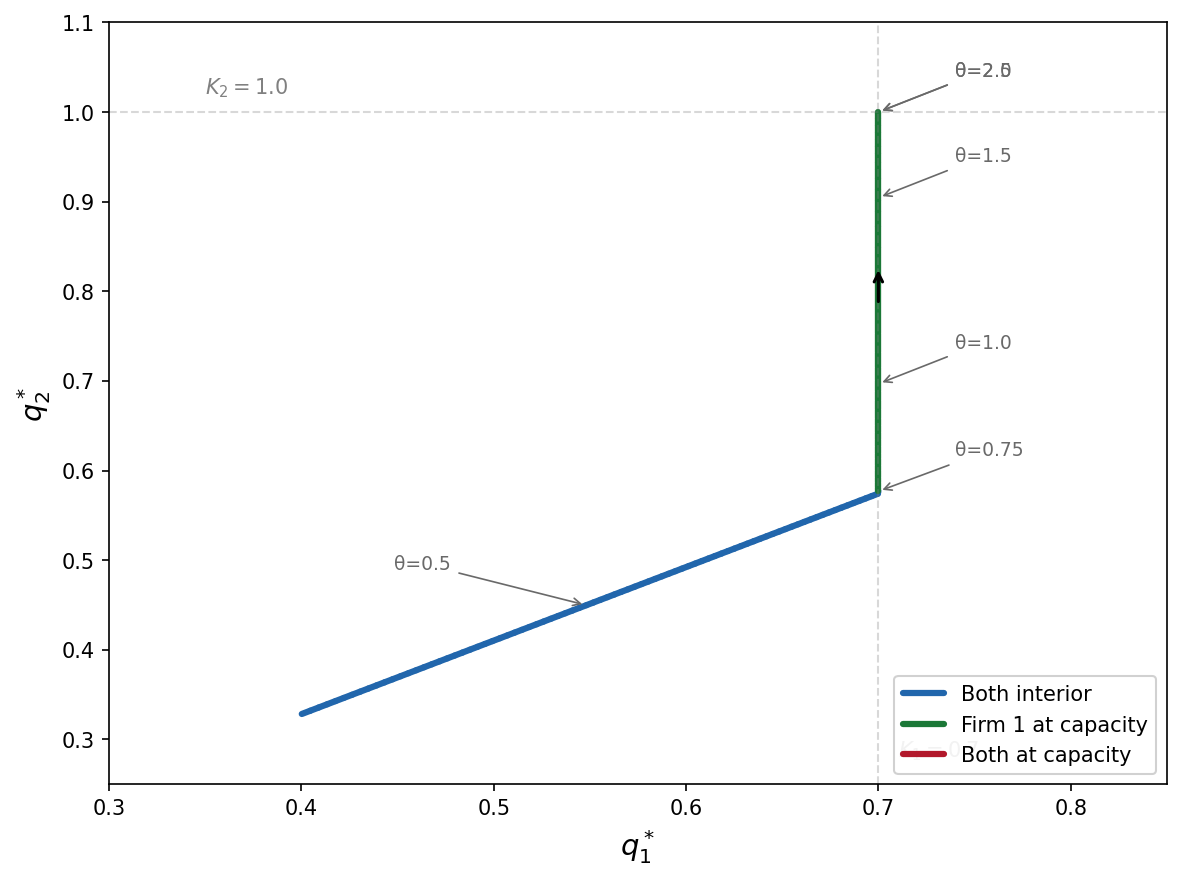

The kinks in the equilibrium paths correspond to transitions between regimes where different capacity constraints become binding

Takeaways from this example

CP conditions arise naturally from constrained optimization: the KKT conditions of the firms’ problems are exactly the CP conditions

Sign conventions matter: mcpsolve uses a different sign convention from the standard KKT formulation. Always check the documentation and verify the solution makes economic sense

The CP framework handles regime changes automatically: as \(\theta\) varies, the solver transitions between interior and corner solutions without us having to enumerate cases manually