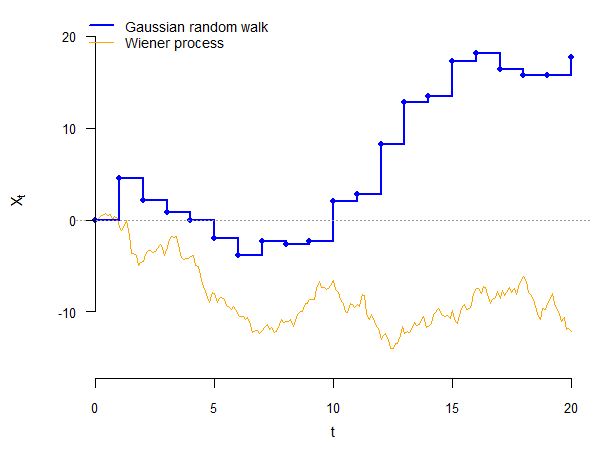

class: center, inverse, middle <style>.xe__progress-bar__container { top:0; opacity: 1; position:absolute; right:0; left: 0; } .xe__progress-bar { height: 0.25em; background-color: #808080; width: calc(var(--slide-current) / var(--slide-total) * 100%); } .remark-visible .xe__progress-bar { animation: xe__progress-bar__wipe 200ms forwards; animation-timing-function: cubic-bezier(.86,0,.07,1); } @keyframes xe__progress-bar__wipe { 0% { width: calc(var(--slide-previous) / var(--slide-total) * 100%); } 100% { width: calc(var(--slide-current) / var(--slide-total) * 100%); } }</style> <style type="text/css"> .pull-left { float: left; width: 44%; } .pull-right { float: right; width: 44%; } .pull-right ~ p { clear: both; } .pull-left-wide { float: left; width: 66%; } .pull-right-wide { float: right; width: 66%; } .pull-right-wide ~ p { clear: both; } .pull-left-narrow { float: left; width: 30%; } .pull-right-narrow { float: right; width: 30%; } .tiny123 { font-size: 0.40em; } .small123 { font-size: 0.80em; } .large123 { font-size: 2em; } .red { color: red } .orange { color: orange } .green { color: green } </style> # Statistics ## Stochastic processes ### (Chapter 7) ### Christian Vedel,<br>Department of Economics<br>University of Southern Denmark ### Email: [christian-vs@sam.sdu.dk](mailto:christian-vs@sam.sdu.dk) ### Updated 2026-04-06 --- class: middle # Today's lecture .pull-left-wide[ **Modelling random phenomena that evolve over time** - **Section 1:** Stochastic processes — definition and sample paths - **Section 2:** Transformations — partial sums and first differences - **Section 3:** States and waiting times - **Section 4:** Bernoulli and binomial processes - **Section 5:** Poisson process - **Section 6:** Gaussian random walk - **Section 7:** Wiener process (Brownian motion) ] .pull-right-narrow[  ] --- # Why stochastic processes? .pull-left-wide[ - Economic variables evolve over time: GDP growth, interest rates, exchange rates, asset prices - **Time series econometrics** builds formal probability models for these sequences - The processes covered today are the *building blocks* for some of the most important models in economics and finance ] -- .pull-left-wide[ - The next two slides show exactly where this leads ] -- .pull-left-wide[ > .orange[**Heads up:** the mathematics on the next slides will look unfamiliar — that is intentional. You are **not** expected to understand it now. Return to it after the course and notice how much has clicked into place.] ] --- # What you are building towards: time series .pull-left-wide[ > .orange[**Preview only — no need to understand this now**] ] .pull-left-wide[ The workhorse model of time series econometrics is the **AR(1)**: `$$Y_t = \mu + \rho \, Y_{t-1} + \varepsilon_t, \qquad \varepsilon_t \overset{iid}{\sim} \mathcal{N}(0,\sigma^2)$$` ] -- .pull-left-wide[ The parameter `\(\rho\)` determines everything: | `\(\rho\)` | Process | Consequence | |:---:|:---|:---| | `\(abs(\rho) < 1\)` | Stationary — mean-reverting | Standard regression is valid | | `\(\rho = 1\)` | **Gaussian random walk** with drift | Spurious regression — `\(R^2 \to 1\)` even for unrelated series | | `\(abs(\rho) > 1\)` | Explosive | Variance grows without bound | ] -- .pull-right-narrow[ - Deciding which case applies requires knowing what a random walk *is* — and how to test for one (**unit root tests**, e.g., Augmented Dickey–Fuller) - You will encounter all of this in later courses ] --- # What you are building towards: finance .pull-left-wide[ > .orange[**Preview only — no need to understand this now**] ] .pull-left-wide[ Stock prices are modelled as **geometric Brownian motion**: `$$dS_t = \mu \, S_t \, dt + \sigma \, S_t \, dW_t$$` where `\(W_t\)` is a **Wiener process** — the continuous-time process you will meet today ] -- .pull-left-wide[ - The **Black–Scholes** option pricing formula is a direct consequence of this model - Every modern derivatives textbook starts from `\(dW_t\)` ] --- # What you are building towards: Markov chains .pull-left-wide[ > .orange[**Preview only — no need to understand this now**] ] .pull-left-wide[ Today's lecture also lays the groundwork for **Markov chains** — processes where the future depends *only* on the current state, not the full history: `$$P(Z_{t+1} = j \mid Z_t = i, Z_{t-1}, \ldots) = P(Z_{t+1} = j \mid Z_t = i)$$` ] -- .pull-left-wide[ - Markov chains are used in macroeconomic models of recessions, credit-rating transitions, and job search theory - They also underlie many machine learning algorithms and reinforcement learning ] --- class: inverse, middle, center # Stochastic processes --- # Time dimension .pull-left-wide[ - Often, uncertain situations involve a time dimension (e.g., the evolution of a stock price over time) ] -- .pull-left-wide[ - Let us consider a simple example: every morning, we toss a fair coin ] --- # Tossing a coin .pull-left-wide[ - Let `\(Z_t\)` be the random variable indicating the outcome of the `\(t\)`-th coin toss: `$$Z_t = \begin{cases} 0, & \text{tails on toss } t \\ 1, & \text{heads on toss } t \end{cases}$$` ] -- .pull-left-wide[ - We may be interested in several aspects of this: - how many times did heads appear in a year, on average? - what is the probability of getting heads (or tails) for a whole week in a row? - how many tosses can we expect between two heads? ] --- # Stochastic process .pull-left-wide[ > A **stochastic process** `\(\{Z_t, t \in T\}\)` is a collection of random variables `\(Z_t\)` indexed by time `\(t\)`, which belongs to the index set `\(T\)`. > > The outcome of a stochastic process, `\(\{z_t, t \in T\}\)`, is called a **realization** or a **sample path**. > > The outcome `\(z_t\)` of one of the random variables `\(Z_t\)` in a stochastic process is called an **incident**. ] -- .pull-left-wide[ - Like random variables, stochastic processes are *functions* that assign a random variable `\(Z_t\)` to a point in time `\(t\)` ] -- .pull-left-wide[ - Same as with random variables, stochastic processes can be of two types: - in *discrete time*, if the index set `\(T\)` is countable (finite or infinite) - in *continuous time*, if the index set `\(T\)` is uncountable (infinite) ] --- # Stochastic process .pull-left-wide[ - Suppose that we follow our couple for a week, so `\(T = \{ 1, 2, \ldots, 7 \}\)` - A realization may be: `$$z = \{1, 0, 0, 1, 1, 1, 0 \}$$` - That is, `\(z_1 = 1\)`, `\(z_2 = 0\)`, `\(z_3 = 0\)`, ..., `\(z_7 = 0\)` ] -- .pull-left-wide[ - Same as we could assign probabilities to random variables, we can also assign probabilities to stochastic processes - In this case, it is the probability of a certain realization (sample path) ] -- .pull-left-wide[ - In our example, if the coin tosses are independent, the probability of each sample path is `\(0.5^7 = 0.0078\)` (because there are `\(2^7\)` possible paths, all with equal probability) ] --- # .red[Practice 1: Stochastic processes] .pull-left-wide[ **1.** Consider the coin-toss example with `\(T = \{1, 2, 3\}\)` and `\(p = 0.5\)`. a) How many possible sample paths are there? b) What is the probability of the sample path `\(z = \{1, 1, 0\}\)`? **2.** A student records whether it rains (`\(Z_t = 1\)`) or not (`\(Z_t = 0\)`) each day for 5 days. Assume each day is independent with `\(p = 0.3\)`. a) What is the probability of the sample path `\(z = \{0, 0, 0, 0, 0\}\)`? ] --- class: inverse, middle, center # Transformations of a stochastic process --- # Partial sum .pull-left-wide[ - One advantage to working with stochastic processes is that we can use them to model real-life events - Transformations make our job even easier ] -- .pull-left-wide[ - For example, suppose you want to count how many times heads appeared until a certain toss - We can define the random variable `\(X_t\)` as: `$$X_t = Z_1 + Z_2 + \ldots + Z_t = \sum_{s=1}^t Z_s$$` ] -- .pull-left-wide[ - The stochastic process `\(\{ X_t, t \in T \}\)` is a **partial sum transformation** of the initial stochastic process `\(\{Z_t, t \in T\}\)` - In our example, we would have `\(x = \{ 1, 1, 1, 2, 3, 4, 4 \}\)` ] --- # Other transformations .pull-left-wide[ - Another useful transformation is the **first-difference**, which shows the change in a stochastic process from one period to the next (e.g., change in income) ] -- .pull-left-wide[ - This can be done in absolute terms: `$$X_t = \Delta Z_t = Z_t - Z_{t-1}$$` ] -- .pull-left-wide[ - It can also be done in relative terms (e.g., inflation rate): `$$X_t = \frac{Z_t - Z_{t-1}}{Z_{t-1}}$$` ] -- .pull-left-wide[ - Note that in both of these cases, the transformed stochastic process is "shorter" by one period (`\(t\)` starts at 2!) ] --- # .red[Practice 2: Transformations] .pull-left-wide[ Consider the realization `\(z = \{2, 5, 3, 8, 6\}\)` for `\(t = 1, 2, 3, 4, 5\)`. **1.** Compute the partial sum process `\(x_t = \sum_{s=1}^t z_s\)` for `\(t = 1, \ldots, 5\)`. **2.** Compute the absolute first-difference `\(x_t = z_t - z_{t-1}\)` for `\(t = 2, \ldots, 5\)`. **3.** Compute the relative first-difference `\(x_t = \frac{z_t - z_{t-1}}{z_{t-1}}\)` for `\(t = 2, \ldots, 5\)`. **4.** Why does the first-difference process have one fewer observation than the original? ] --- # .red[Raise your hand 1: Transformations] <div class="countdown" id="timer_44257925" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** Consider `\(z = \{3, 1, 4, 1\}\)`. What is the partial sum `\(x_3\)`? - **A)** 4 — the value of `\(z_3\)` - **B)** 8 — the sum of the first 3 values - **C)** 9 — the sum of all 4 values ] -- .pull-left-wide[ **Q2.** A realization is `\(z = \{4, 2, 8, 5\}\)`. What is the absolute first-difference `\(\Delta z_4 = z_4 - z_3\)`? - **A)** 5 — the level at `\(t = 4\)` - **B)** `\(-3\)` — the change from `\(t = 3\)` to `\(t = 4\)` - **C)** 3 — the absolute value of the change ] --- class: inverse, middle, center # States and waiting times --- # States .pull-left-wide[ - One aspect of a stochastic process that is particularly interesting is its state at a certain point in time - The **state** of a stochastic process at time `\(t\)` is given by the random variable representing the value taken at time `\(t\)` ] -- .pull-left-wide[ - In our example, consider the partial sum transformation `\(\{ X_t, t \in T \}\)` - The state of this process at time `\(t_0 = 2\)` is simply `\(X_2\)` ] --- # State distribution .pull-left-wide[ - Note that `\(X_2\)` (the sum of `\(Z_1\)` and `\(Z_2\)`) can take three values: 0, 1, or 2, with probabilities: `$$f(0) = P(Z_1 = 0, Z_2 = 0) = 0.25$$` `$$f(1) = P(Z_1 = 0, Z_2 = 1) + P(Z_1 = 1, Z_2 = 0) = 0.5$$` `$$f(2) = P(Z_1 = 1, Z_2 = 1) = 0.25$$` ] -- .pull-left-wide[ - The distribution of `\(X_2\)` is called the **state distribution** of the stochastic process at time 2 ] -- .pull-left-wide[ - This also shows the usefulness of stochastic processes: instead of directly specifying the distribution of the number of times heads appeared, we can use a stochastic process - This approach is more intuitive and often easier ] --- # Waiting time .pull-left-wide[ - Another interesting aspect of a stochastic process is the **waiting time**, i.e., the time it will take until a particular state is reached (or passed) for the first time ] -- .pull-left-wide[ - For example, we may want to know how long it takes until heads appears twice - Since the stochastic process consists of random variables, the time until one particular state is realized is also random ] -- .pull-left-wide[ - Let `\(Y_2\)` be the random variable indicating how long it takes until heads appears twice ] --- # Waiting-time distribution .pull-left-wide[ - The distribution of the random variable `\(Y_2\)` is called a **waiting-time distribution** - In our example, `\(Y_2\)` can take the values 2, 3, ..., 7 ] -- .pull-left-wide[ - We can then calculate probabilities for these values. For example: - `\(f(2)\)`: `\(Y_2 = 2\)` if `\(Z_1 = 1\)` and `\(Z_2 = 1\)`, which can happen with probability 0.25 - `\(f(3)\)`: `\(Y_2 = 3\)` if: - `\(Z_1 = 1\)`, `\(Z_2 = 0\)`, and `\(Z_3 = 1\)`, which occurs with probability 0.125 - `\(Z_1 = 0\)`, `\(Z_2 = 1\)`, and `\(Z_3 = 1\)`, which occurs with probability 0.125 - `\(\Rightarrow\)` `\(f(3) = 2 \cdot 0.125 = 0.25\)` ] -- .pull-left-wide[ - Note that the stochastic process may not be "long enough" for us to observe the desired value - In this case, we can calculate `\(1 - F(7)\)` and/or `\(1 - F(6)\)` ] --- # Types of processes .pull-left-wide[ .small123[ | | Discrete State | Continuous State | |---|:---:|:---:| | **Discrete Time** | Bernoulli, Binomial | Gaussian random walk | | **Continuous Time** | Poisson | Wiener | ] ] --- # .red[Practice 3: States and waiting times] .pull-left-wide[ A quality inspector checks items on a production line. Each item is defective with probability `\(p = 0.3\)`, independently. Let `\(X_t\)` be the number of defective items found by inspection `\(t\)`. **1.** Find the state distribution of `\(X_4\)` — compute `\(f(0)\)`, `\(f(1)\)`, `\(f(2)\)`. **2.** Let `\(Y_1\)` be the waiting time until the first defective item is found. Compute `\(f(1)\)`, `\(f(2)\)`, `\(f(3)\)`. **3.** What is `\(1 - F(3)\)` for `\(Y_1\)`? What does this represent in the context of quality control? ] --- class: inverse, middle, center # The Bernoulli process and the binomial process --- # The Bernoulli process .pull-left-wide[ > A **Bernoulli process** `\(\{Z_t, t \in T \}\)` satisfies the following conditions: > > 1. Time: `\(T = \{ 1, 2, 3, \ldots \}\)` > > 2. State: `\(Z_t \in \{ 0, 1 \}\)` for all `\(t\)` > > 3. Distribution of outcomes: each state follows a Bernoulli distribution with parameter `\(p\)` > > 4. Relationship between outcomes: each state is independent of the other states: `\(Z_t\)` and `\(Z_s\)` are independent for all `\(s \not= t\)` ] --- # The Bernoulli process .pull-left-wide[ - The Bernoulli process is characterized by the fact that, at each point in time, an incident can either occur (`\(Z_t = 1\)`) or not (`\(Z_t = 0\)`) - This means that an element from a Bernoulli population is drawn at each point in time ] -- .pull-left-wide[ - Our previous example (coin toss) is a Bernoulli process with `\(p = 0.5\)` ] --- # Example of path of a Bernoulli process (`\(p = 0.5\)`) .center[  ] --- # The binomial process .pull-left-wide[ - Sometimes, what is of interest is the number of events in a Bernoulli process - As before, we can obtain this using the partial sum transformation: `$$X_t = \sum_{s=1}^t Z_s$$` ] -- .pull-left-wide[ - This is a sum of independent Bernoulli-distributed random variables, which yields a binomial process ] --- # The binomial process .pull-left-wide[ > A **binomial process** `\(\{X_t, t \in T \}\)` satisfies the following conditions: > > 1. Time: `\(T = \{ 1, 2, 3, \ldots \}\)` > > 2. State: `\(X_t \in \{ 0, 1, \ldots, t \}\)` for all `\(t\)` > > 3. Distribution of outcomes: states are such that `\((X_{t+n} - X_t)\)` follows a binomial distribution with parameters `\(n\)` and `\(p\)`, for all `\(n\)` and `\(t\)`, and `\(X_0 = 0\)` > > 4. Relationship between outcomes: `\((X_{t_1} - X_{t_2})\)` and `\((X_{t_3} - X_{t_4})\)` are independent, for all `\(t_1 > t_2 > t_3 > t_4\)` ] --- # Example of path of a binomial process (`\(p = 0.5\)`) .center[  ] --- # The binomial process .pull-left-wide[ - With a binomial process, the probability of a certain number of events in a time interval depends on the *length* of the time interval and not on *when* this time interval occurs ] -- .pull-left-wide[ - In addition, the number of events in a time interval is independent of the number of events in any other non-overlapping time interval ] -- .pull-left-wide[ - A binomial process is a **counting process**: it models the number of events that occurred up to a certain point in time ] --- # State distribution of a binomial process .pull-left-wide[ - Using the definition of the binomial process, we can easily see that: `$$X_t - X_0 = X_t \sim Bin(t, p)$$` - This gives us the state distribution of the binomial process ] -- .pull-left-wide[ - We can therefore determine the probability function of `\(X_t\)`: `$$f(x) = {t \choose x} \cdot p^x \cdot (1 - p)^{t-x}$$` ] -- .pull-left-wide[ - The expected value and variance of `\(X_t\)` also come from the binomial distribution: `$$E(X_t) = t \cdot p \qquad Var(X_t) = t \cdot p \cdot (1 - p)$$` ] .pull-right-narrow[ *Coin toss:* The number of heads after `\(t\)` fair coin tosses follows `\(Bin(t,\; 0.5)\)`. ] --- # Waiting-time distribution of a binomial process .pull-left-wide[ - As before, let `\(Y_{x_0}\)` be the time until `\(X_t = x_0\)` for the first time - The distribution of `\(Y_{x_0}\)` is called the **negative binomial distribution**: `$$Y_{x_0} \sim Negbin(x_0, p)$$` ] -- .pull-left-wide[ - The probability function of `\(Y_{x_0}\)` is: `$$f(y) = {{y - 1} \choose {x_0 - 1}} \cdot p^{x_0} \cdot (1 - p)^{y - x_0}$$` ] -- .pull-left-wide[ - The expected value and variance of `\(Y_{x_0}\)` are: `$$E(Y_{x_0}) = \frac{x_0}{p} \qquad Var(Y_{x_0}) = x_0 \cdot \frac{1 - p}{p^2}$$` ] .pull-right-narrow[ *Coin toss:* The number of tosses needed to get `\(x_0\)` heads follows `\(Negbin(x_0,\; 0.5)\)`. ] --- # Waiting-time distribution of a binomial process .pull-left-wide[ - We can also ask: what is the time until the first event occurs? - This is a negative binomial distribution with parameters 1 and `\(p\)` ] -- .pull-left-wide[ - This distribution is also very useful and has its own name: the **geometric distribution**: `$$Y_{1} \sim Negbin(1, p) = Geo(p)$$` ] -- .pull-left-wide[ - The probability function for the geometric distribution is: `$$f(y) = p \cdot (1 - p)^{y - 1}$$` - This distribution also represents the distribution of the waiting time until the next event occurs ] .pull-right-narrow[ *Coin toss:* The number of fair coin tosses until the first head follows `\(Geo(0.5)\)`. ] --- # .red[Practice 4: Bernoulli and binomial processes] .pull-left-wide[ A website receives visits according to a Bernoulli process with `\(p = 0.4\)` per minute. **1.** What is `\(f(3)\)` — the probability of exactly 3 visits in the first 8 minutes? **2.** What are `\(E(X_8)\)` and `\(Var(X_8)\)`? **3.** What is the probability that the first visit occurs on minute 4? Use the geometric distribution. **4.** What is the expected waiting time until the 2nd visit? ] --- # .red[Raise your hand 2: Bernoulli and binomial processes] <div class="countdown" id="timer_db820a0c" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** A binomial process has `\(p = 0.3\)` and `\(t = 10\)`. What is `\(E(X_{10})\)`? - **A)** 0.3 — the probability of success - **B)** 3 — expected count of events - **C)** 7 — expected number of non-events ] -- .pull-left-wide[ **Q2.** The waiting time until the *first* event in a Bernoulli process follows which distribution? - **A)** Binomial — counts the total number of events in a fixed number of trials - **B)** Geometric — special case of negative binomial with `\(x_0 = 1\)` - **C)** Negative binomial — the general distribution for waiting times in a binomial process ] --- class: inverse, middle, center # The Poisson process --- # The Poisson process .pull-left-wide[ > A **Poisson process** `\(\{X_t, t \in T \}\)` satisfies the following conditions: > > 1. Time: `\(T = (0, \infty)\)` > > 2. State: `\(X_t \in \{ 0, 1, 2, \ldots \}\)` for all `\(t\)` > > 3. Distribution of outcomes: states are such that `\((X_{t + \tau} - X_t)\)` follows a Poisson distribution with parameter `\((\lambda \cdot \tau)\)`, for all `\(\tau\)` and `\(t\)`, and `\(X_0 = 0\)` > > 4. Relationship between outcomes: `\((X_{t_1} - X_{t_2})\)` and `\((X_{t_3} - X_{t_4})\)` are independent, for all `\(t_1 > t_2 > t_3 > t_4\)` ] --- # The Poisson process .pull-left-wide[ - The Poisson process gives the number of events that have occurred up to a given point in time - Therefore, it is also a counting process, but in continuous time ] -- .pull-left-wide[ - Note that the number of events occurring in any time interval of length `\(\tau\)` follows a Poisson distribution with parameter `\(\lambda \cdot \tau\)`, meaning that only the *length* of the interval matters, not *when* the time interval starts ] --- # State distribution of a Poisson process .pull-left-wide[ - Using the definition of the Poisson process, we can easily see that: `$$X_t - X_0 = X_t \sim Poisson(\lambda \cdot t)$$` - This gives us the state distribution of the Poisson process as a Poisson distribution ] -- .pull-left-wide[ - We can therefore determine the probability function of `\(X_t\)`: `$$f(x) = \frac{(\lambda \cdot t)^x}{x!} \cdot e^{-(\lambda \cdot t)}$$` ] -- .pull-left-wide[ - The expected value and variance of `\(X_t\)` also come from the Poisson distribution: `$$E(X_t) = \lambda \cdot t \qquad Var(X_t) = \lambda \cdot t$$` ] --- # Probability updating in a Poisson process .pull-left-wide[ - If we know that `\(b\)` events occurred until time `\(s\)`, we can update the probability that `\(x\)` events will occur until time `\(t\)`: `$$f(x \mid X_s = b) = P(X_t - X_s = x - b)$$` ] -- .pull-left-wide[ - But we know that `\(X_t - X_s\)` follows a Poisson distribution with parameter `\(\lambda \cdot (t - s)\)` - Therefore, the conditional probability function becomes: `$$f(x \mid X_s = b) = \frac{[\lambda \cdot (t - s)]^{x - b}}{(x - b)!} \cdot e^{-[\lambda \cdot (t-s)]}$$` ] --- # Waiting-time distribution of a Poisson process .pull-left-wide[ - As before, let `\(Y_{x_0}\)` be the time until `\(X_t = x_0\)` for the first time - The distribution of `\(Y_{x_0}\)` is called the **Erlang distribution**: `$$Y_{x_0} \sim Erlang(\lambda, x_0)$$` ] -- .pull-left-wide[ - The probability function of `\(Y_{x_0}\)` is: `$$f(y) = \frac{\lambda^{x_0} \cdot y^{x_0 - 1}}{(x_0 - 1)!} \cdot e^{-\lambda \cdot y}$$` ] -- .pull-left-wide[ - The expected value and variance of `\(Y_{x_0}\)` are: `$$E(Y_{x_0}) = \frac{x_0}{\lambda} \qquad Var(Y_{x_0}) = \frac{x_0}{\lambda^2}$$` ] .footnote[ .small123[After Danish statistician Agner Krarup Erlang: https://en.wikipedia.org/wiki/Agner_Krarup_Erlang] ] --- # Waiting-time distribution of a Poisson process .pull-left-wide[ - We can also ask: what is the time until the first (or the next) event occurs? - This is an Erlang distribution with parameters `\(\lambda\)` and 1 ] -- .pull-left-wide[ - This distribution is also quite useful and has its own name: the **exponential distribution**: `$$Y_{1} \sim Erlang(1, \lambda) = Exp(\lambda)$$` ] -- .pull-left-wide[ - The probability function for the exponential distribution is: `$$f(y) = \lambda \cdot e^{-\lambda \cdot y}$$` ] --- # .red[Practice 5: Poisson process] .pull-left-wide[ Customers arrive at a shop according to a Poisson process with rate `\(\lambda = 3\)` per hour. **1.** What is `\(f(5)\)` — the probability that exactly 5 customers arrive in the first 2 hours? **2.** What are `\(E(X_2)\)` and `\(Var(X_2)\)`? **3.** If 4 customers arrived by hour 1, what is `\(f(x \mid X_1 = 4)\)` for the number arriving by hour 2? **4.** What is the expected waiting time until the 3rd customer arrives? ] --- # .red[Raise your hand 3: Poisson process] <div class="countdown" id="timer_c18fd52d" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** A Poisson process has `\(\lambda = 4\)` per hour. What is `\(Var(X_3)\)`? - **A)** 4 — the rate parameter `\(\lambda\)` - **B)** 12 — `\(\lambda \cdot t\)` - **C)** 16 — `\(\lambda^2\)` ] -- .pull-left-wide[ **Q2.** 10 customers arrived in the first 2 hours of a Poisson process with `\(\lambda = 3\)`. How are the arrivals in the *next* hour distributed? - **A)** Poisson(3) — non-overlapping intervals are independent - **B)** Poisson(13) — adding the 10 existing arrivals to `\(\lambda\)` - **C)** Poisson(5) — because 10 customers arrived in 2 hours, suggesting a rate of 5 per hour ] --- class: inverse, middle, center # The Gaussian random walk --- # The Gaussian random walk .pull-left-wide[ > A **Gaussian random walk** `\(\{X_t, t \in T \}\)` satisfies the following conditions: > > 1. Time: `\(T = \{ 1, 2, 3, \ldots \}\)` > > 2. State: `\(X_t \in (-\infty, \infty)\)` for all `\(t\)` > > 3. Distribution of outcomes: states are such that `\((X_{t + n} - X_t)\)` follows a Normal distribution with mean `\(n \cdot \mu\)` and variance `\(n \cdot \sigma^2\)`, for all `\(n\)` and `\(t\)`; and `\(X_0 = 0\)` > > 4. Relationship between outcomes: `\((X_{t_1} - X_{t_2})\)` and `\((X_{t_3} - X_{t_4})\)` are independent, for all `\(t_1 > t_2 > t_3 > t_4\)` ] -- .pull-left-wide[ - `\(\mu\)` is called the **drift** parameter and `\(\sigma^2\)` the **diffusion** parameter ] --- # The Gaussian random walk .pull-left-wide[ - A random walk is a partial sum of independent and identically distributed random variables (e.g., the binomial process is a random walk) - The Gaussian random walk is a continuous-state discrete-time process ] -- .pull-left-wide[ - It represents the "drunken walk:" each step can occur in a random direction, either forwards or backwards - The change in this process, at any point in time, is normally distributed with mean and variance that depend on the *length* of the time interval but not on *when* the interval starts ] --- # State distribution of a Gaussian random walk .pull-left-wide[ - Using the definition of the Gaussian random walk, we can easily see that: `$$X_t - X_0 = X_t \sim \mathcal{N}(t \cdot \mu, t \cdot \sigma^2)$$` - This gives us the state distribution of the Gaussian random walk as a normal distribution ] -- .pull-left-wide[ - We can therefore determine the probability density function of `\(X_t\)`: `$$f(x) = \frac{1}{ \sigma \cdot \sqrt{2 \cdot \pi \cdot t }} \cdot e^{- \frac{(x - t \cdot \mu)^2}{2 \cdot t \cdot \sigma^2}}$$` ] -- .pull-left-wide[ - The expected value and variance of `\(X_t\)` also come from the normal distribution: `$$E(X_t) = t \cdot \mu \qquad Var(X_t) = t \cdot \sigma^2$$` ] --- # Probability updating in a Gaussian random walk .pull-left-wide[ - Same as in the case of a Poisson process, we can calculate the conditional CDF of `\(X_t\)` given that `\(X_s = b\)`: `$$F(x \mid X_s = b) = P(X_t - X_s \leq x - b)$$` ] -- .pull-left-wide[ - But we know that `\(X_t - X_s\)` follows a normal distribution with mean `\((t - s) \cdot \mu\)` and variance `\((t - s) \cdot \sigma^2\)` - Therefore, the conditional CDF can be derived from the normal distribution `\(\mathcal{N}((t - s) \cdot \mu, (t - s) \cdot \sigma^2)\)`: `$$F(x \mid X_s = b) = \Phi \left( \frac{(x - b) - (t - s) \cdot \mu}{\sqrt{(t - s) \cdot \sigma^2}} \right)$$` ] --- class: inverse, middle, center # The Wiener process --- # The Wiener process .pull-left-wide[ > A **Wiener process** (**Brownian motion**) `\(\{X_t, t \in T \}\)` satisfies the following conditions: > > 1. Time: `\(T = (0, \infty)\)` > > 2. State: `\(X_t \in (-\infty, \infty)\)` for all `\(t\)` > > 3. Distribution of outcomes: states are such that `\((X_{t + \tau} - X_t)\)` follows a Normal distribution with mean `\(\tau \cdot \mu\)` and variance `\(\tau \cdot \sigma^2\)`, for all `\(\tau\)` and `\(t\)`; and `\(X_0 = 0\)` > > 4. Relationship between outcomes: `\((X_{t_1} - X_{t_2})\)` and `\((X_{t_3} - X_{t_4})\)` are independent, for all `\(t_1 > t_2 > t_3 > t_4\)` ] --- # The Wiener process vs Gaussian random walk .pull-left-wide[ - The Wiener process is very similar to a Gaussian random walk, except that it takes place in continuous time ] -- .pull-left-wide[ - In other words, the Gaussian random walk only changes at certain points in time (positive integers), while the Wiener process changes continuously ] --- # Example of path of a Gaussian random walk and of a Wiener process (`\(\mu = 0\)`, `\(\sigma^2 = 4\)`) .center[  ] --- # State distribution of a Wiener process .pull-left-wide[ - The state distribution of a Wiener process is completely identical to the state distribution of a Gaussian random walk: `$$X_t - X_0 = X_t \sim \mathcal{N}(t \cdot \mu, t \cdot \sigma^2)$$` ] -- .pull-left-wide[ - With probability density function: `$$f(x) = \frac{1}{ \sigma \cdot \sqrt{2 \cdot \pi \cdot t }} \cdot e^{- \frac{(x - t \cdot \mu)^2}{2 \cdot t \cdot \sigma^2}}$$` ] -- .pull-left-wide[ - The expected value and variance of `\(X_t\)` are: `$$E(X_t) = t \cdot \mu \qquad Var(X_t) = t \cdot \sigma^2$$` ] --- # Waiting-time distribution of a Wiener process .pull-left-wide[ - As before, let `\(Y_{x_0}\)` be the time until `\(X_t = x_0\)` for the first time - The distribution of `\(Y_{x_0}\)` is called the **inverse Gaussian distribution**, or the **Wald distribution**: `$$Y_{x_0} \sim IG \left( \frac{x_0}{\mu}, \frac{x_0^2}{\sigma^2} \right)$$` ] -- .pull-left-wide[ - The expected value and variance of `\(Y_{x_0}\)` are: `$$E(Y_{x_0}) = \frac{x_0}{\mu} \qquad Var(Y_{x_0}) = \frac{x_0}{\mu} \cdot \frac{\sigma^2}{\mu^2}$$` ] --- # .red[Practice 6: Gaussian random walk and Wiener process] .pull-left-wide[ A stock price follows a Gaussian random walk with `\(\mu = 0.1\)` and `\(\sigma^2 = 1\)`. **1.** What is the distribution of `\(X_{10}\)`? Give the mean and variance. **2.** If `\(X_5 = 3\)`, what is the conditional distribution of `\(X_{10}\)`? **3.** Compute `\(F(4 \mid X_5 = 3)\)` — the probability that `\(X_{10} \leq 4\)` given `\(X_5 = 3\)`. **4.** How does the Wiener process differ from the Gaussian random walk? What stays the same? ] --- # .red[Raise your hand 4: Poisson and Gaussian] <div class="countdown" id="timer_f83bcad9" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** A Poisson process has `\(\lambda = 2\)` per hour. What is `\(E(X_3)\)`? - **A)** 2 — the rate parameter - **B)** 6 — rate times time - **C)** 0.5 — the mean waiting time until the first event ] -- .pull-left-wide[ **Q2.** A Gaussian random walk has `\(\mu = 0\)` and `\(\sigma^2 = 1\)`. What is `\(Var(X_4)\)`? - **A)** 1 — the diffusion parameter - **B)** 2 — square root of 4 - **C)** 4 — variance scales with time ] --- # Before next time .pull-left[ - Read the assigned reading - Next time: The sampling process .red[We will do things with numbers from the real world!!] ] .pull-right[  ]