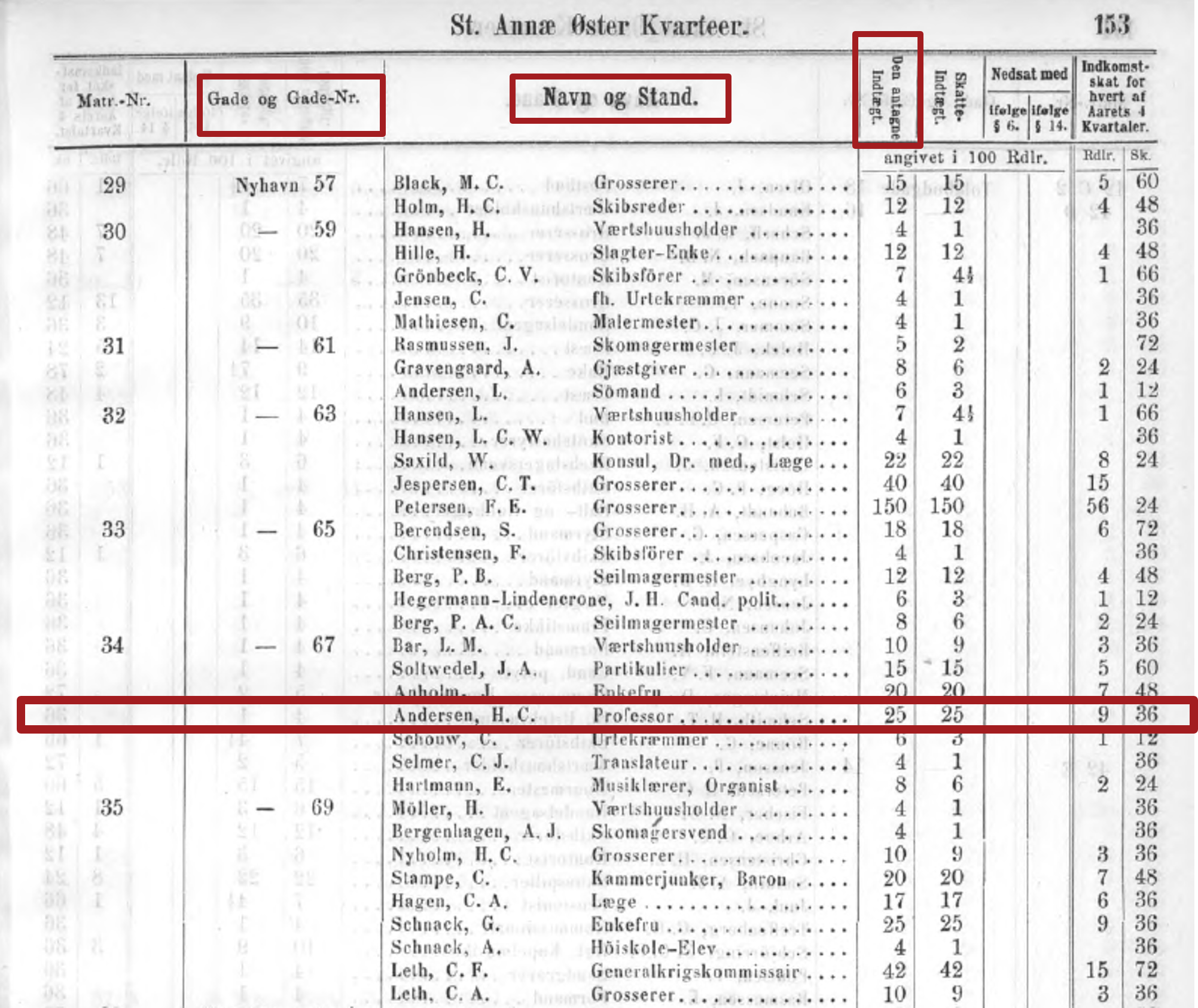

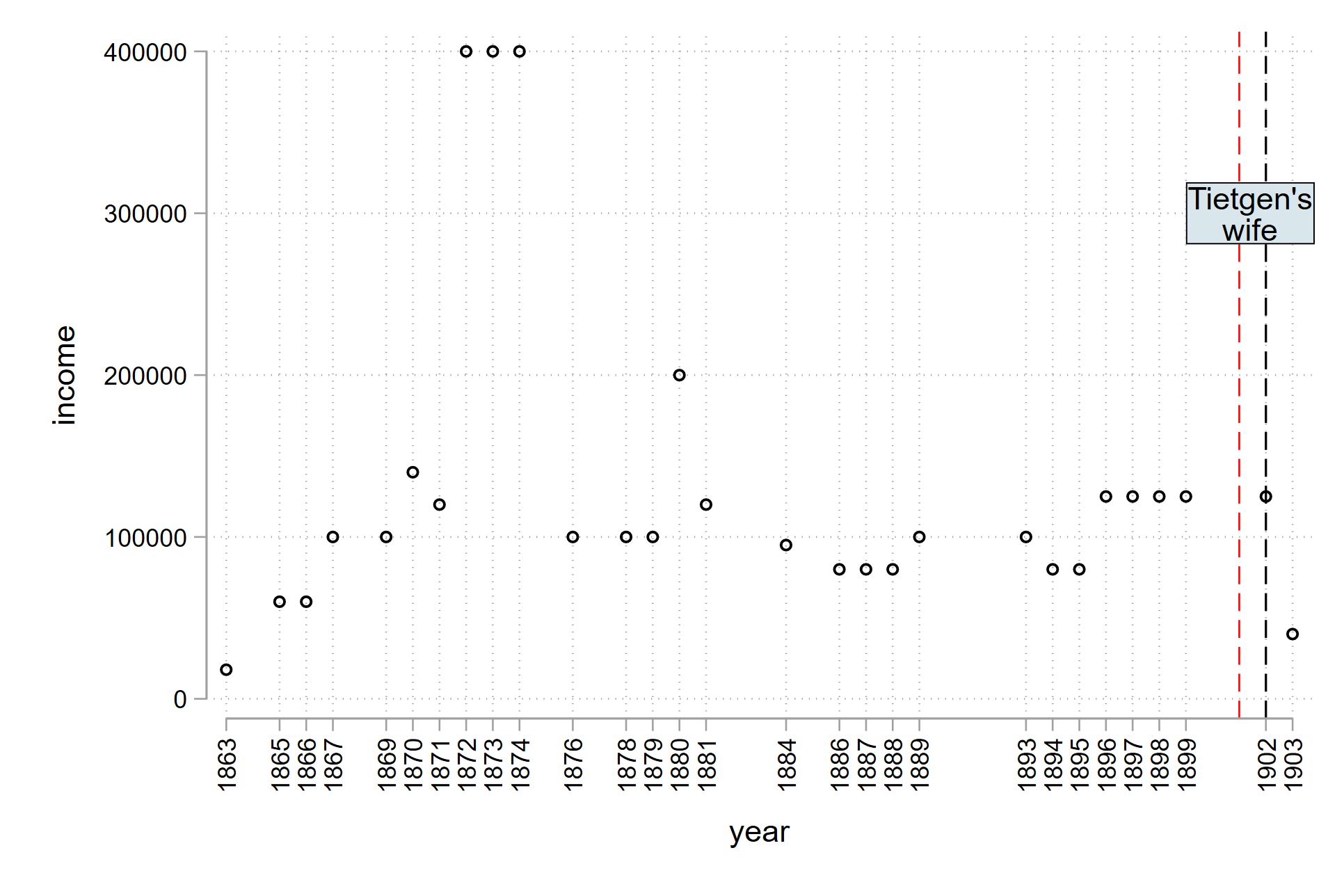

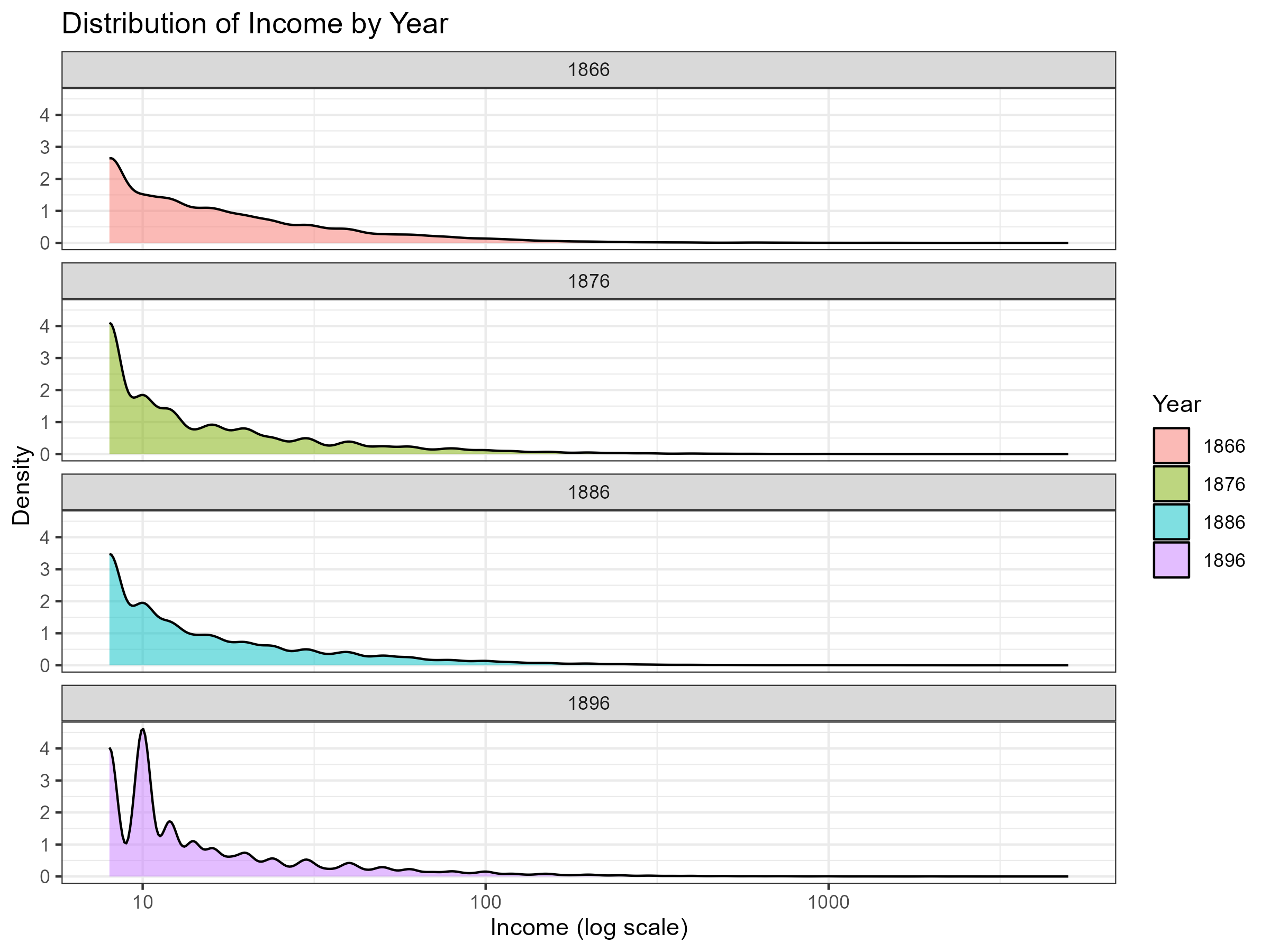

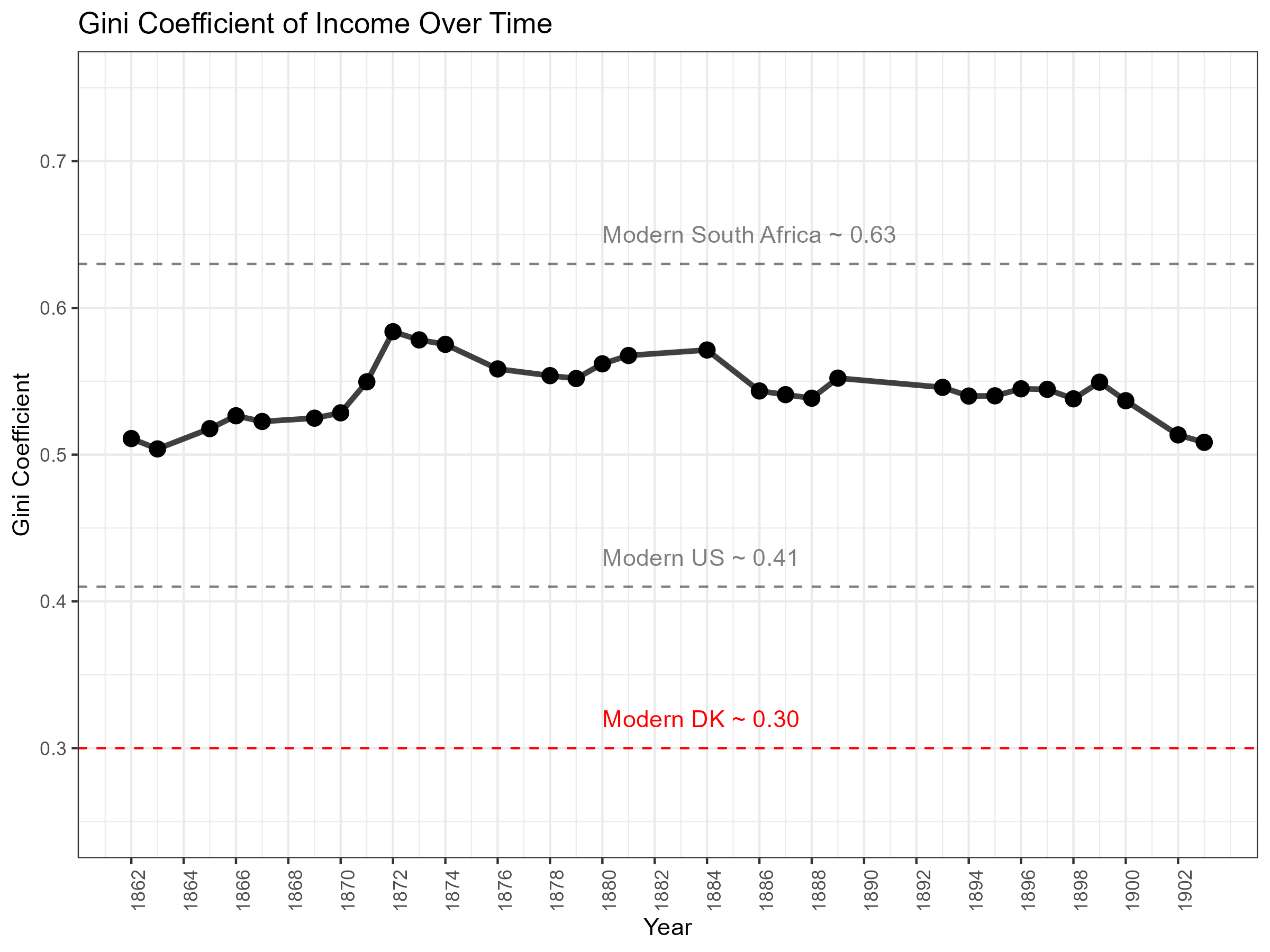

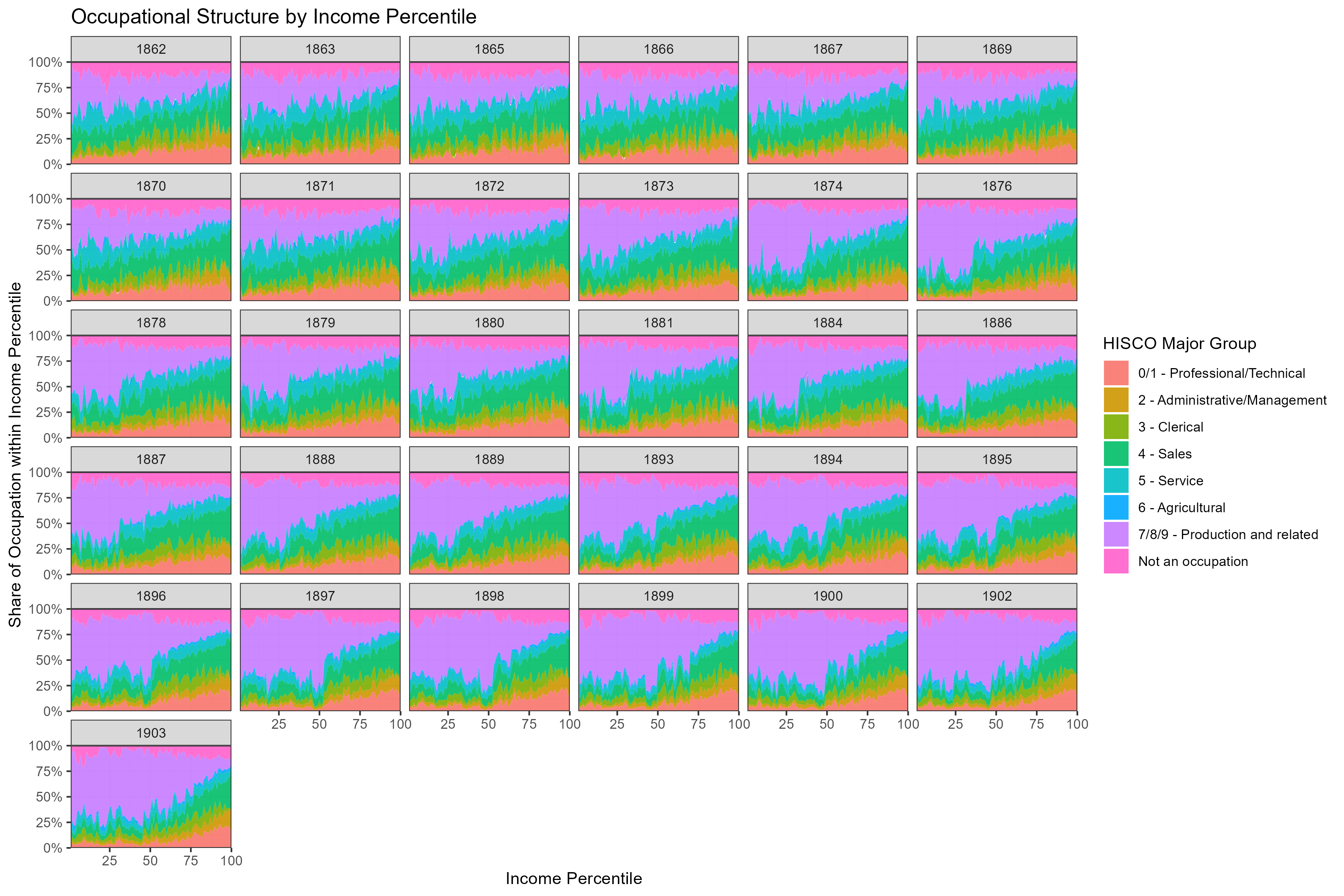

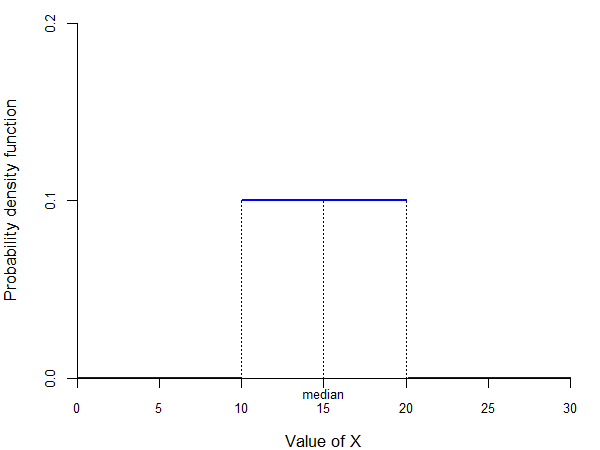

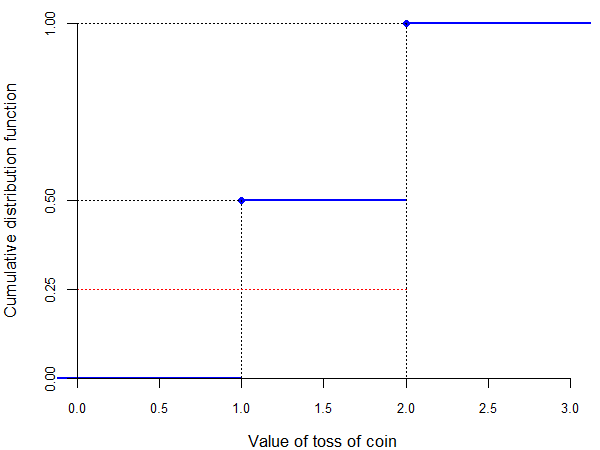

class: center, inverse, middle <style>.xe__progress-bar__container { top:0; opacity: 1; position:absolute; right:0; left: 0; } .xe__progress-bar { height: 0.25em; background-color: #808080; width: calc(var(--slide-current) / var(--slide-total) * 100%); } .remark-visible .xe__progress-bar { animation: xe__progress-bar__wipe 200ms forwards; animation-timing-function: cubic-bezier(.86,0,.07,1); } @keyframes xe__progress-bar__wipe { 0% { width: calc(var(--slide-previous) / var(--slide-total) * 100%); } 100% { width: calc(var(--slide-current) / var(--slide-total) * 100%); } }</style> <style type="text/css"> .pull-left { float: left; width: 44%; } .pull-right { float: right; width: 44%; } .pull-right ~ p { clear: both; } .pull-left-wide { float: left; width: 66%; } .pull-right-wide { float: right; width: 66%; } .pull-right-wide ~ p { clear: both; } .pull-left-narrow { float: left; width: 30%; } .pull-right-narrow { float: right; width: 30%; } .tiny123 { font-size: 0.40em; } .small123 { font-size: 0.80em; } .large123 { font-size: 2em; } .red { color: red } .orange { color: orange } .green { color: green } </style> # Statistics ## Descriptive measures ### (Chapter 5) ### Christian Vedel,<br>Department of Economics<br>University of Southern Denmark ### Email: [christian-vs@sam.sdu.dk](mailto:christian-vs@sam.sdu.dk) ### Updated 2026-03-06 --- class: middle # This lecture .pull-left-wide[ **Descriptive measures summarize the key features of a random variable's distribution.** - **Moments:** Expected value, variance, standard deviation, and higher moments - **Quantiles:** Median, quartiles, percentiles - **Choosing measures:** When to use the mean vs. median vs. mode - **Relationships:** Covariance and correlation between random variables ] .pull-right-narrow[  ] --- class: inverse, middle, center # Descriptive measures and random variables --- # The nice problem: too much data -- .pull-left-wide[ - Sometimes as researchers we face a surprisingly nice problem: **we have too much data** .center[ ### Two routes ] .pull-left[ - Pick a few observations and learn everything about them - Shoe size - Pet's name - *everything* - But only for a few ] .pull-right[ - Compute summaries of the data - Average shoe size - Most common pet's name - But for all ] ] -- .pull-right-narrow[ - As economists, we are often in the business of **drawing inference about hypotheses from summaries** - This is hard — because summarizing means **losing information** - The art is choosing summaries that lose as little *relevant* information as possible ] -- .pull-left-wide[ *The rest of your statistics journey is somehow dedicated to fancy summaries of data.* ] --- # Copenhagen tax records, 1863–1904 .pull-left[ - We are digitizing **individual-level tax records** from Copenhagen covering 1863–1904 - Currently **1,291,023 observations** — every taxable resident: name, income, address, occupation - This data basically does not exist in the same quality anywhere else going this far back - Enables research on income inequality, social mobility, long-run development, etc. - .small123[*Ongoing research - this is a peak into the the machinery of research in progress*] ] .pull-right[  .small123[*Original tax ledger, Copenhagen 1863*] ] --- # C.E. Frijs (1817–1896) .pull-left-wide[ - Part of the landed nobility — Prime Minister (1865–1870) - **Income: 500,000 kr/year (1869–1872)** - Equivalent to roughly 50 million kr today - Highest recorded income in Copenhagen at the time - Occupation in the books: *Konseilspræsident* (1869), *Lensgreve* (1871) - Residence: Toldbodvej 26 ] .pull-right-narrow[  .small123[*Source: Wikipedia*] ] --- # H.C. Andersen (1805–1875) .pull-left-wide[ - Renowned Danish fairy-tale author - **Income: 3,600 kr (1865) → 4,000 kr (1869–1874)** - Placed him in the **top 20%** of income earners in Copenhagen - Occupation in the books: *Professor* (1865), *Etatsraad* (1869) - Residence: Nyhavn 67 (1865) → Lille Kongensgade 1 (1869) → Høibroplads 21 (1870) ] .pull-right-narrow[  .small123[*Source: Wikipedia*] ] --- # C.F. Tietgen (1829–1901) .pull-left-wide[ - Prominent banker and industrialist — born into modest circumstances in Odense - Moved to Copenhagen in 1855 (after 5 years in Manchester) - Director of *Privatbanken* (1857); played a central role in founding: - Kjøbenhavns Sporvei-Selskab (1866) - Det Store Nordiske Telegraf-Selskab (1869) - Burmeister & Wain (1871), Tuborgs Bryggerier (1873) - His life-cycle earnings are on the next slide → ] .pull-right-narrow[  .small123[*Source: Wikipedia*] ] --- # C.F. Tietgen — life-cycle earnings .pull-left-wide[  ] --- # What can we say about this distribution? .pull-left[ - We are looking at a **subsection of 136,506 observations** from the records - It's kernel density estimate of the probability density function of income in Copenhagen in 1866, 1876, 1886, and 1896 (you'll learn more about those later) - Basically, you are looking at the *distribution* of income in Copenhagen at four points in time - **How do we summarize what we see?** `\(\Rightarrow\)` this is exactly what descriptive measures are for ] .pull-right[  ] -- .pull-left-wide[ - You already know these: mean, median, standard deviation, quantiles, etc. - **Now it's time to relearn them** ] --- # Summary statistics tell us something .pull-left-wide[ | Year | n | Mean | SD | Median | Max | |------|----:|-----:|---:|-------:|----:| | 1866 | 17,793 | 26 | 59 | 12 | 3,000 | | 1876 | 29,063 | 25 | 77 | 12 | 5,000 | | 1886 | 38,606 | 25 | 61 | 12 | 3,000 | | 1896 | 50,105 | 25 | 64 | 10 | 2,500 | .small123[*Incomes in historical units. SD = standard deviation.* - The **mean is more than twice the median** — the distribution is strongly right-skewed (a few very rich pull the mean up) - The **standard deviation is larger than the mean** — enormous spread around the average - The **median is remarkably stable** — (speculation) as Denmark industrialized, more people got rich, but a similar amount entered the labour force, echoing the "Engel's pause" hypothesis of stagnant living standards for the working class during early industrialization ] ] --- # Ongoing research: what else can we learn? .pull-left[ **Income inequality over time**  .small123[*Gini coefficient in Copenhagen, 1863–1904*] ] .pull-right[ **Which occupations earned what?**  .small123[*Which occupations in which part of the income distribution?**] ] .footnote[ .small123[ `\(^*\)`*The occupational classification is based on the HISCO system. HISCO coded using *OccCANINE* (Dahl, Johansen, Vedel, 2024)* ] ] --- # Descriptive measures .pull-left-wide[ Two types: - **Moments** — based on weighted averages (mean income, average height) - **Quantiles** — based on splitting the distribution (richest 10%, median earner) ] --- # Moments: an example .pull-left-wide[ - **Mean income in 1866 Copenhagen = 26 kr** `$$E(X) = \int_{-\infty}^\infty x \cdot f(x) \, dx$$` - But **median = 12 kr** — Frijs's 500,000 kr pulls the mean far above what most people earned ] .pull-right-narrow[  ] --- # Quantiles: an example .pull-left-wide[ - **Median income = 12 kr** splits the distribution in half: 50% earn less, 50% earn more - Other examples: `\(q_{0.9}\)` = income threshold for the top 10%; `\(q_{0.25}\)` = bottom quarter cutoff - **Key advantage**: quantiles are robust — Frijs's 500,000 kr does not move the median ] --- # Descriptive measures and random variables .pull-left-wide[ - Let `\(X\)` = income of a randomly chosen Copenhagener in 1866 - `\(f(12)\)` = probability density at 12 kr, reflecting how common that income level is in the population - Applying descriptive measures to `\(X\)` gives us information about the **underlying population** ] --- # .red[Raise your hand 1: Moments or quantiles?] <div class="countdown" id="timer_f3f975ba" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** "The average (mean) income in Denmark is 450,000 DKK per year." This is: - **A)** A moment — it is based on a weighted average of values - **B)** A quantile — it describes who earns above/below a threshold - **C)** Neither — it is just a descriptive number, not a formal measure ] -- .pull-left-wide[ **Q2.** "The bottom 25% of Danish earners earn less than 280,000 DKK per year." This is: - **A)** A moment — it uses averages over the whole distribution - **B)** A quantile — it identifies a split point of the distribution - **C)** A variance — it describes the spread of the income distribution ] --- # Distribution .pull-left-wide[ > **Distribution** = the list of probabilities associated with the values that a random variable can take (if discrete) or the probability density function (if continuous) - The distribution of the random variable is a representation of the distribution of the underlying population - Therefore, we call the distribution of the random variable the **population distribution** - Similarly, we call the descriptive measures for the random variable the **population measures** - This is in contrast with averages and other descriptive measures calculated in a sample, which are **sample measures** ] --- # Distribution — example .pull-left-wide[ - Let `\(X\)` = income of a randomly chosen Copenhagener in 1866 - The **population distribution** of `\(X\)` is the full probability density function over all possible incomes — the smooth curve you would get if you knew every single person's income - In practice we never observe the full population — we observe a **sample** of `\(n = 17{,}793\)` people - From this sample we compute **sample measures**: e.g., sample mean `\(\bar{x} = 26\)` kr, sample median `\(= 12\)` kr - These are estimates of the unknown **population measures** `\(E(X)\)` and `\(q_{0.5}\)` - The kernel density plot is our best approximation of the population distribution from the sample ] .pull-right-narrow[  .small123[*Estimated population distribution of income, 1866*] ] --- # .red[Practice 1: Descriptive measures and distributions] .pull-left-wide[ **Q1.** Classify each statement as a *moment*, a *quantile*, or neither: - "The average exam score is 62 out of 100" - "Half of students score below 58" - "The most common score is 70" **Q2.** A researcher models the wage `\(W\)` of a randomly chosen Danish worker as a continuous random variable. Is the distribution of `\(W\)` a population or a sample distribution? **Q3.** A handful of workers earn over 500,000 DKK/month while most earn 30,000–50,000 DKK. Would you expect `\(E(W)\)` or the median of `\(W\)` to be higher? Why? ] --- class: inverse, middle, center # Moments --- # Expected value of discrete random variables .pull-left-wide[ > The **expected value (mean value)** of a discrete random variable `\(X\)` with probability function `\(f(x)\)` is given by: > `$$E(X) = \sum_{i=1}^N x_i f(x_i) = x_1 f(x_1) + x_2 f(x_2) + \ldots + x_N f(x_N) = \mu$$` > where `\(x_1, x_2, \ldots, x_N\)` are all the different values that `\(X\)` can take. - The expected value is also called "mean" and denoted by `\(\mu\)` (*mu*) - For example, the expected value of a dice roll is: `$$E(X) = 1 \cdot \frac{1}{6} + 2 \cdot \frac{1}{6} + \ldots + 6 \cdot \frac{1}{6} = 3.5$$` ] --- # Expected value of discrete random variables .pull-left-wide[ - Note that 3.5 is *not* one of the possible values of `\(X\)` `\(\Rightarrow\)` how do we interpret this expected value? ] -- .pull-left-wide[ - Imagine that you play a game where you win one krone for each dot on the face of the dice (so, if you roll a 4, you win 4 kroner) - The expected value of 3.5 tells you that, if you play this game 10 times, you should expect to win about 35 kroner (3.5 times 10) - In this case, the expected value is the "average win per play" ] -- .pull-left-wide[ - Intuitively, the expected value is the average of all the values obtained if you were to repeat the experiment generating `\(X\)` an infinite number of times - Another interpretation of the average value is the "center of mass" ] --- # Properties of the expected value .pull-left-wide[ - Let `\(h(\cdot)\)` be a function, `\(a\)` and `\(b\)` be **constants** (i.e., real numbers), and `\(X\)` a random variable (continuous or discrete). Then: 1. The expected value of `\(h(X)\)` is given by: `$$E[h(X)] = \sum_{i=1}^N h(x_i) f(x_i) = h(x_1) f(x_1) + h(x_2) f(x_2) + \ldots + h(x_N) f(x_N)$$` 2. `\(E(a) = a\)` 3. `\(E(aX) = a E(X)\)` 4. `\(E(a + X) = a + E(X)\)` 5. `\(E(a + b X) = a + b E(X)\)` - Important: note that, in general, `\(E[h(X)] \not= h[E(X)]\)` ] --- # .red[Practice 2: Expected value] .pull-left-wide[ A fair 4-sided die shows values 1, 2, 3, 4 with equal probability `\(\frac{1}{4}\)`. **Q1.** Calculate `\(E(X)\)`. **Q2.** You win `\(X^2\)` kroner per roll. Calculate your expected winnings `\(E(X^2)\)`. **Q3.** Is `\(E(X^2) = [E(X)]^2\)`? What does this tell you about applying functions to expected values? ] --- # .red[Raise your hand 2: Interpreting the expected value] <div class="countdown" id="timer_ce88d1f2" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** A fair die is rolled once. `\(E(X) = 3.5\)`. What does this mean? - **A)** 3.5 is the most likely outcome of a single roll - **B)** 3.5 is the long-run average if you roll very many times - **C)** 3.5 is always between the minimum (1) and maximum (6), so it is a "middle" value ] -- .pull-left-wide[ **Q2.** `\(E(X) = 5\)` and `\(E(Y) = 3\)`. What is `\(E(2X - Y + 4)\)`? - **A)** `\(2 \cdot 5 - 3 + 4 = 11\)` - **B)** `\(2 \cdot 5 - 3 = 7\)` - **C)** Cannot be determined without knowing if `\(X\)` and `\(Y\)` are independent ] --- # Expected value of continuous random variables .pull-left-wide[ - Recall that we defined concepts related to continuous random variables in ways similar to discrete random variables, by making two changes: - replace the probability function with the probability density function - replace summations with integrals > The **expected value (mean value)** of a continuous random variable `\(X\)` with probability density function `\(f(x)\)` is given by: > `$$E(X) = \int_{-\infty}^\infty x f(x) \, dx = \mu$$` ] --- # A challenge: Expected value of discrete random variables .pull-left-wide[ - Consider the following two games related to the toss of a coin: - you win 1 krone if "heads," you lose 1 krone if "tails" - you win 10 kroner if "heads," you lose 10 kroner if "tails" - Let `\(X\)` be the random variable representing the first game and `\(Y\)` the random variable representing the second game - The possible values of `\(X\)` are `\(-1\)` and `\(1\)`, each with probability 50% - The possible values of `\(Y\)` are `\(-10\)` and `\(10\)`, each with probability 50% - Their expected values are: `$$E(X) = 1 \cdot \frac{1}{2} + (-1) \cdot \frac{1}{2} = 0$$` `$$E(Y) = 10 \cdot \frac{1}{2} + (-10) \cdot \frac{1}{2} = 0$$` - But are they similarly "risky"? Can we get a better measure? ] --- # Variance .pull-left-wide[ > The **variance** of a random variable `\(X\)` is usually denoted by `\(\sigma^2\)` (*sigma squared*) and is defined as: > `$$Var(X) = E \left( \left[ X - E(X) \right]^2 \right) = \sigma^2$$` > > If `\(X\)` is a discrete random variable with probability function `\(f(x)\)`, then: > `$$Var(X) = \sum_{i=1}^N (x_i - \mu)^2 f(x_i)$$` > > If `\(X\)` is a continuous random variable with probability density function `\(f(x)\)`, then: > `$$Var(X) = \int_{-\infty}^\infty (x - \mu)^2 f(x) \, dx$$` ] --- # Variance .pull-left-wide[ - Intuitively, the variance is a measure of how "spread out" is the distribution of a random variable - In our example, we have: `$$Var(X) = (1 - 0)^2 \cdot \frac{1}{2} + (-1 - 0)^2 \cdot \frac{1}{2} = 1$$` `$$Var(Y) = (10 - 0)^2 \cdot \frac{1}{2} + (-10 - 0)^2 \cdot \frac{1}{2} = 100$$` - So we see that `\(Y\)` is more "spread out" than `\(X\)` ] --- # .red[Practice 3: Variance] .pull-left-wide[ Using the same two coin-flip games: `\(X\)` wins ±1 and `\(Y\)` wins ±10, each with probability ½. **Q1.** Confirm that `\(E(X) = E(Y) = 0\)`. Does the expected value distinguish these two games? **Q2.** Calculate `\(Var(X)\)` and `\(Var(Y)\)`. Which game is riskier? **Q3.** A third game: `\(Z = 5X\)`. Without recalculating from scratch, what is `\(Var(Z)\)`? ] --- # Standard deviation .pull-left-wide[ - One problem with the variance is that the unit of measurement is not the same as that of the random variable - In our example, `\(X\)` is measured in kroner, but `\(Var(X)\)` is measured in kroner squared - It would be useful to have a measure of the spread expressed in the same units of measurement as the random variable > The **standard deviation** of a random variable `\(X\)` is defined as: > `$$\sigma(X) = \sqrt{Var(X)} = \sqrt{\sigma^2}$$` ] --- # Properties of the variance and of the standard deviation -- - The variance and standard deviation have the following properties: .pull-left[ **Variance:** 1. `\(Var(a) = 0\)` 2. `\(Var(aX) = a^2 Var(X)\)` 3. `\(Var(a + X) = Var(X)\)` 4. `\(Var(a + b X) = b^2 Var(X)\)` ] .pull-right[ **Standard deviation:** - `\(\Rightarrow\)` `\(\sigma(a) = 0\)` - `\(\Rightarrow\)` `\(\sigma(aX) = |a| \sigma(X)\)` - `\(\Rightarrow\)` `\(\sigma(a + X) = \sigma(X)\)` - `\(\Rightarrow\)` `\(\sigma(a + b X) = |b| \sigma(X)\)` ] --- # Higher order moments .pull-left-wide[ - Note that the variance is defined as the expected value of the square of the "demeaned" version of `\(X\)` - We can similarly define the expected value of the `\(k\)`-th power of `\(X\)` or of the "demeaned" version of `\(X\)` > The **k-th moment** of a random variable `\(X\)` is defined as: > `$$m_k(X) = E(X^k)$$` > > The **k-th central moment** of `\(X\)` is defined as: > `$$m_k^*(X) = E\left( [X - E(X)]^k \right)$$` ] --- # Higher order moments .pull-left-wide[ - Note that: - the expected value is the first moment of `\(X\)`: `$$E(X) = m_1(X)$$` - the variance is the second central moment of `\(X\)`: `$$Var(X) = m_2^*(X)$$` - Some other useful moments are: - `\(m_3^*(X)\)` describes how skewed is the distribution of `\(X\)` - `\(m_4^*(X)\)` shows how likely are the extreme values of `\(X\)` ] --- class: middle # Higher order moments > Sometimes a moment does not exist. This can lead to trouble. --- # Higher order moments — the St. Petersburg paradox .pull-left-wide[ **The St. Petersburg game:** - A fair coin is tossed until the first heads appears - If the first heads comes on toss `\(N\)`, the payoff is `\(X = 2^N\)` kr. - Since the coin is fair, `$$f(N=n)=2^{-n}, \qquad n=1,2,\ldots$$` ] -- .pull-left-wide[ **The paradox:** - The initial stake is 2 kr., doubled every time heads appears - Your expected winnings are: $$ `\begin{align} E(X) &= 2 \cdot \tfrac{1}{2} + 4 \cdot \tfrac{1}{4} + 8 \cdot \tfrac{1}{8} + \ldots \\ &= 1 + 1 + 1 + \ldots \\ &= \infty \end{align}` $$ - You should be willing to pay any finite amount to play this game. Right? ] -- .pull-right-narrow[  ] --- # Higher order moments — resolution .pull-left-wide[ **What the paradox reveals:** - Expected value theory says you should pay *any* finite price to play — but nobody would pay, say, 1,000,000 kr. - The `\(\infty\)` is driven entirely by vanishingly rare, astronomically large payoffs - With probability `\(\frac{1}{2}\)` you win just 2 kr.; with probability `\(\frac{3}{4}\)` you win at most 4 kr. - The "average" is completely disconnected from what typically happens **The resolution:** - More about this in your *Strategy and Markets* course. ] --- # .red[Practice 4: Expected value and variance] .pull-left-wide[ A random variable `\(X\)` represents the number of heads in two fair coin tosses. It takes values `\(0, 1, 2\)` with probabilities `\(\frac{1}{4}, \frac{1}{2}, \frac{1}{4}\)`. **Q1.** Calculate `\(E(X)\)`. **Q2.** Calculate `\(Var(X)\)`. **Q3.** Let `\(Y = 3X + 2\)`. What are `\(E(Y)\)` and `\(Var(Y)\)`? ] --- # .red[Raise your hand 3: Expected value and variance] <div class="countdown" id="timer_0235b042" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** In general, is `\(E[X^2] = [E(X)]^2\)`? - **A)** Yes, always — the expectation operator is linear - **B)** No, not in general — `\(E[X^2] \geq [E(X)]^2\)` by Jensen's inequality - **C)** Yes, if `\(X\)` is symmetric around zero ] -- .pull-left-wide[ **Q2.** `\(Var(X) = 4\)`. You define `\(Y = -2X + 5\)`. What is `\(Var(Y)\)`? - **A)** `\(Var(Y) = -16\)` — the negative sign flips the variance - **B)** `\(Var(Y) = 16\)` — variance uses `\((-2)^2 = 4\)` - **C)** `\(Var(Y) = 9\)` — adding 5 increases the variance ] --- class: inverse, middle, center # Quantiles --- # Quantiles .pull-left-wide[ - Quantiles represent another way of summarizing the distribution of `\(X\)` - The distribution of income tends to be highly asymmetric - As a result, the mean is not particularly informative - A measure more common in the study of skewed distributions such as the income distribution is the median - Intuitively, the **median** is the value of `\(X\)` that splits the distribution in half ] --- # Median .center[  ] --- # Quantiles .pull-left-wide[ - In general, we can define a quantile for any split of the distribution of `\(X\)` - The intuition is that the 25-th quantile splits the distribution into 25% to the left, 75% to the right - However, the distribution of discrete random variables may not allow such a "nice" split (e.g., we cannot exactly split the distribution of the toss of a coin this way) - Hence, we need to define the quantile in a more convoluted way ] --- # Quantiles .pull-left-wide[ > The **p-quantile** of a random variable `\(X\)` with cumulative distribution function `\(F(x)\)` is the value `\(q_p\)` such that: > - `\(P(X < q_p) \leq p\)` > - `\(P(X > q_p) \leq 1 - p\)` > > If `\(X\)` is a continuous random variable, this simplifies to: > `$$F(q_p) = p$$` - For a continuous random variable, the `\(p\)`-quantile is the value that splits the distribution into `\(p\)` to the left and `\(1 - p\)` to the right - For a discrete random variable, the `\(p\)`-quantile is the value where the cumulative distribution function "jumps" from a value lower than `\(p\)` to one higher than `\(p\)` ] --- # Quantiles for discrete random variables .center[  ] --- # Multiple quantiles .pull-left-wide[ - Unlike moments, quantiles *always* exist - However, they do not have to be unique - For example, it can happen that the random variable `\(X\)` has a distribution with more than one median - In this case, the convention is to use the midpoint of the interval as the median ] --- # Multiple quantiles .center[  ] --- # Multiple quantiles .center[  ] --- # Special names for quantiles .pull-left-wide[ - Some particular quantiles have special names: - `\(q_{0.5}\)` is called the **median** - `\(q_{0.25}\)` and `\(q_{0.75}\)` are called **quartiles** - `\(q_{0.1}, q_{0.2}, \ldots, q_{0.9}\)` are called **deciles** - `\(q_{0.01}, q_{0.02}, \ldots, q_{0.99}\)` are called **percentiles** ] --- # .red[Practice 5: Quantiles] .pull-left-wide[ A discrete random variable `\(X\)` takes values `\(1, 2, 3, 4, 5\)` with equal probability `\(\frac{1}{5}\)`. **Q1.** What is the median of `\(X\)`? **Q2.** What is `\(q_{0.8}\)` (the 80th percentile) of `\(X\)`? **Q3.** A second variable `\(Y\)` takes the same values but with probabilities `\(0.1, 0.1, 0.6, 0.1, 0.1\)`. What is the median of `\(Y\)`? Do moments or quantiles better distinguish `\(X\)` from `\(Y\)`? ] --- # .red[Raise your hand 4: Mean vs. median] <div class="countdown" id="timer_92d9f182" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** Income in a country is heavily right-skewed (a few very high earners). Which measure best describes the "typical" income? - **A)** The mean — it is a moment and uses all the data - **B)** The median — it is a quantile and is robust to extreme values - **C)** The variance — it captures how unequal incomes are ] -- .pull-left-wide[ **Q2.** A distribution has median 50 and mean 80. What can you conclude? - **A)** The distribution is left-skewed (long left tail pulls mean below median) - **B)** The distribution is right-skewed (long right tail pulls mean above median) - **C)** There must be measurement errors in the data ] --- class: inverse, middle, center # Choice of descriptive measures --- # Choice of descriptive measures .pull-left-wide[ - Imagine that you want to study the distribution of income in the Danish population - Let `\(X\)` be the income of a randomly chosen individual `\(\Rightarrow\)` the probability function of `\(X\)` should represent the distribution of income in Denmark - What can we tell from the fact that the *expected value* of `\(X\)` is high? - the *average* person has a high income - but this does not mean that *everyone* has a high income: we could have two groups of people, one really rich and one really poor - What can we tell if the *median* value of `\(X\)` is high? - the person in the middle of the distribution of income has a high income - but this again does not mean that *everyone* has a high income: we could still have two groups of people, one really rich and one really poor, with a single person in the middle ] --- # Choice of descriptive measures .center[  ] --- # Choice of descriptive measures .pull-left-wide[ - What the expected value and the median have in common is that they both describe the *central tendency* of the distribution - They give the best description of the "typical" observation (expected value) or of the "middle" of the distribution (median) - If the distribution is symmetric, then the median and the expected value are equal - However, the median is generally more *robust* to measurement errors (e.g., if there are small errors in how incomes are inputted) ] --- # Mode .pull-left-wide[ - Another commonly used descriptive measure is the mode > The **mode (modal value)** of a random variable `\(X\)` is the value `\(x_m\)` where the probability (density) function attains its maximum. That is: > `$$f(x_m) \geq f(x)$$` > for all possible values of `\(x\)`. - Like the quantiles, the mode always exists but does not have to be unique - A distribution is *unimodal* if it has only one mode, or *bimodal* if it has two - We can identify the mode(s) as the "peak(s)" of the probability (density) function ] --- # .red[Practice 6: Choosing descriptive measures] .pull-left-wide[ For each scenario, state which descriptive measure(s) you would use and why. **Scenario A:** You want to report the "typical" apartment price in Copenhagen, where a few luxury properties sell for 50M+ DKK. **Scenario B:** You analyse exam scores (0–100) and want to summarize both the average performance and the risk of scoring below 40. **Scenario C:** You study the most frequently occurring party affiliation in a large survey. ] --- # .red[Raise your hand 5: Choosing descriptive measures] <div class="countdown" id="timer_fe09fd64" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** For a strictly symmetric distribution, which must be true? - **A)** Mean = Median = Mode always - **B)** Mean = Median, but mode may differ - **C)** All three are equal only if the distribution is normal ] -- .pull-left-wide[ **Q2.** A distribution is bimodal. This means: - **A)** The mean and median are both equal to one of the two modes - **B)** The probability (density) function has two local maxima - **C)** The variance is exactly twice as large as for a unimodal distribution ] --- class: inverse, middle, center # Descriptive measures for the relationship between random variables --- # Descriptive measures for the relationship between random variables .pull-left-wide[ - We sometimes need to know how two random variables are related - For example, suppose you invest in two different stocks on the stock market - The future price of each stock is a random variable - You would want to know if the prices of the two stocks are likely to move together because this exposes you to more risk: - if both prices go up, you gain more - but if both prices fall, then you lose more - "Don't put all your eggs in one basket:" you may want to invest in stocks whose prices are likely to move in opposite directions ] --- # Expected value of a sum of random variables .pull-left-wide[ - Let us start again with simple descriptive measures of the joint distribution - We previously defined the joint probability (density) function of two random variables `\(X\)` and `\(Y\)` as `\(f(x, y)\)` - Now suppose that you buy `\(a\)` shares of the stock `\(X\)` and `\(b\)` shares of the stock `\(Y\)` - What should you expect as the value of your portfolio? - It should be the expected value of this combination of `\(X\)` and `\(Y\)`: `$$E(aX + bY)$$` ] --- # Expected value of a sum of random variables .pull-left-wide[ > The **expected value of a sum of random variables** `\(X\)` and `\(Y\)` is: > `$$E(aX + bY) = aE(X) + bE(Y)$$` - This formula holds true whether `\(X\)` and `\(Y\)` are discrete or continuous - It also does not depend on whether `\(X\)` and `\(Y\)` move together or not ] --- # Covariance between two random variables .pull-left-wide[ > The **covariance** between two random variables `\(X\)` and `\(Y\)` is defined as: > `$$Cov(X, Y) = E\left( [X - E(X)] [Y - E(Y)] \right) = E \left[ (X - \mu_X)(Y - \mu_Y) \right]$$` > `$$= E(XY) - \mu_X \mu_Y$$` ] --- # Covariance between two random variables .pull-left-wide[ - If `\(X\)` and `\(Y\)` are both discrete, this becomes: `$$Cov(X, Y) = \sum_{i=1}^{N_x} \sum_{j=1}^{N_y} [(x_i - \mu_X) (y_j - \mu_Y) f(x_i, y_j)]$$` `$$= \sum_{i=1}^{N_x} \sum_{j=1}^{N_y} [x_i y_j f(x_i, y_j)] - \mu_X \mu_Y$$` - If `\(X\)` and `\(Y\)` are both continuous, this becomes: `$$Cov(X, Y) = \int_{-\infty}^\infty \int_{-\infty}^\infty (x - \mu_X) (y - \mu_Y) f(x, y) \, dy \, dx$$` `$$= \int_{-\infty}^\infty \int_{-\infty}^\infty x y f(x, y) \, dy \, dx - \mu_X \mu_Y$$` ] --- # Properties of the covariance .pull-left-wide[ - The covariance tells us how the two variables move together: - `\(Cov(X, Y) > 0\)` means that when `\(X\)` is above its mean, then it is likely that `\(Y\)` is also above its mean - `\(Cov(X, Y) < 0\)` means that when `\(X\)` is below its mean, then it is likely that `\(Y\)` is above its mean - The covariance between `\(X\)` and `\(Y\)` has a few useful properties: 1. `\(Cov(X, Y) = Cov(Y, X)\)` 2. `\(Cov(aX, bY) = a b \, Cov(X, Y)\)` 3. `\(Cov(a + X, b + Y) = Cov(X, Y)\)` 4. `\(Cov(X + Z, Y) = Cov(X, Y) + Cov(Z, Y)\)` ] --- # Variance of a sum of random variables .pull-left-wide[ > The **variance of a sum of random variables** `\(X\)` and `\(Y\)` is: > `$$Var(aX + bY) = Var(aX) + Var(bY) + 2 Cov(aX, bY)$$` > `$$= a^2 Var(X) + b^2 Var(Y) + 2 a b \, Cov(X, Y)$$` - If we think of the variance of your earnings as the risk, now you can see why buying two stocks whose prices move in opposite directions helps with the risk - If `\(Cov(X, Y) < 0\)`, then: `$$Var(aX + bY) < Var(aX) + Var(bY)$$` - If the prices of the two stocks move in the same direction, then `\(Cov(X, Y) > 0\)` and: `$$Var(aX + bY) > Var(aX) + Var(bY)$$` ] --- # Correlation coefficient between two random variables .pull-left-wide[ - The covariance has two major disadvantages: - its unit of measurement is the product of the units of measurement of `\(X\)` and `\(Y\)` (in our example, kroner squared) - the value of the covariance is not very informative and is sensitive to changes in the units of measurement of `\(X\)` and `\(Y\)` > The **correlation coefficient** between two random variables `\(X\)` and `\(Y\)` is defined as: > `$$\rho(X, Y) = \frac{Cov(X, Y)}{\sqrt{Var(X) \cdot Var(Y)}} = \frac{Cov(X, Y)}{\sigma(X) \cdot \sigma(Y)}$$` ] --- # Correlation coefficient between two random variables .pull-left-wide[ - The correlation coefficient is always between `\(-1\)` and 1 - The sign and the value indicate the direction and the strength of the relationship between `\(X\)` and `\(Y\)`: - `\(\rho(X, Y) = -1\)` means *perfect negative correlation*: every time `\(X\)` is above its mean, `\(Y\)` is below its mean - `\(-1 < \rho(X, Y) < 0\)` indicates *negative correlation*: when `\(X\)` is above its mean, `\(Y\)` is generally below its mean - `\(\rho(X, Y) = 0\)` means *no correlation*: when `\(X\)` is above its mean, `\(Y\)` is above its mean and below its mean with equal chance - `\(0 < \rho(X, Y) < 1\)` indicates *positive correlation*: when `\(X\)` is above its mean, `\(Y\)` is generally above its mean - `\(\rho(X, Y) = 1\)` means *perfect positive correlation*: every time `\(X\)` is above its mean, `\(Y\)` is also above its mean - Important: if `\(X\)` and `\(Y\)` are independent, then `\(Cov(X, Y) = \rho(X, Y) = 0\)`, but the reverse is **not** true! ] --- # .red[Practice 7: Covariance and correlation] .pull-left-wide[ Two discrete random variables `\(X\)` and `\(Y\)` have the following joint distribution: | | `\(Y = 0\)` | `\(Y = 1\)` | |---|:---:|:---:| | `\(X = 0\)` | 0.3 | 0.2 | | `\(X = 1\)` | 0.2 | 0.3 | **Q1.** Calculate `\(E(X)\)`, `\(E(Y)\)`, `\(Var(X)\)`, `\(Var(Y)\)`. **Q2.** Calculate `\(Cov(X, Y)\)`. **Q3.** Calculate `\(\rho(X, Y)\)` and interpret the sign. ] --- # .red[Raise your hand 6: Correlation and independence] <div class="countdown" id="timer_975a5814" data-update-every="1" tabindex="0" style="top:TRUE;right:0;"> <div class="countdown-controls"><button class="countdown-bump-down">−</button><button class="countdown-bump-up">+</button></div> <code class="countdown-time"><span class="countdown-digits minutes">00</span><span class="countdown-digits colon">:</span><span class="countdown-digits seconds">20</span></code> </div> .pull-left-wide[ **Q1.** `\(X\)` and `\(Y\)` are independent. What is `\(\rho(X, Y)\)`? - **A)** `\(\rho(X, Y) = 0\)` always — independence implies no linear association - **B)** `\(\rho(X, Y)\)` can be anything — independence and correlation are unrelated - **C)** `\(\rho(X, Y) = 1\)` — independent variables move together by definition ] -- .pull-left-wide[ **Q2.** You find `\(\rho(X, Y) = 0\)`. Can you conclude that `\(X\)` and `\(Y\)` are independent? - **A)** Yes — zero correlation means no relationship at all - **B)** No — zero correlation only rules out *linear* dependence - **C)** Yes, if `\(X\)` and `\(Y\)` are jointly normally distributed ] --- # Before next time .pull-left[ - Read the assigned reading - Next time: Commonly used distributions `\(\rightarrow\)` Chapter 6 ] .pull-right[  ]